Can I Open an IRA for My Child? A Parent's Guide

Yes, you absolutely can open an IRA for your child. In fact, it's one of the most powerful financial moves you can make as a parent. There's just one non-negotiable rule you have to follow: your child must have earned income.

This single requirement is the key that unlocks decades of potential tax-advantaged growth, turning their first summer job into a massive head start on their financial future.

The Earned Income Requirement for a Child's IRA

The idea of opening a retirement account for a kid often surprises people, but the IRS is perfectly fine with it. The logic is simple: an Individual Retirement Arrangement (IRA) is for retirement, and retirement savings are tied to work. So, any minor—no matter how young—can have an IRA as long as they have legitimate, earned income.

This is usually where parents pause and ask, "Well, what really counts as earned income?" It’s more than just a formal W-2 from the local ice cream shop. It also includes all those classic childhood side hustles.

A few real-world examples of what the IRS considers earned income for a minor include:

- Babysitting for neighbors on the weekend.

- Mowing lawns or doing yard work for cash.

- Tutoring younger students in subjects they excel at.

- Modeling or acting in local commercials or plays.

- Working as a camp counselor during the summer.

What doesn't count? Allowance, birthday money from Grandma, or investment gains. The money must be paid as compensation for actual work performed.

What Counts as Earned Income for Minors

To make it crystal clear, not all money a child receives is considered "earned" by the IRS. Here's a simple breakdown to help you figure out if your child's income qualifies.

| Income Source | Typically Qualifies? | Key Consideration |

|---|---|---|

| Job with a W-2 | Yes | This is the most straightforward type of earned income. |

| Self-Employment (e.g., babysitting, lawn mowing) | Yes | You must keep records of the work and payment. |

| Acting or Modeling Fees | Yes | This is considered income for services rendered. |

| Allowance | No | It's not tied to specific work performance. |

| Birthday/Holiday Cash Gifts | No | Gifts are not compensation for work. |

| Investment Gains (e.g., stock dividends) | No | This is considered unearned, or investment, income. |

The bottom line is simple: if your child was paid to do a job, that money likely counts. Just be prepared to document it if they're self-employed.

Turning Small Gigs into a Big Future

Here’s where the real magic happens. The IRS rule is straightforward: total IRA contributions for the year cannot be more than the child’s earned income, or the annual IRA limit—whichever is lower.

So, if your 14-year-old earns $3,000 mowing lawns, you can help them fund up to $3,000 into an IRA in their name. Better yet, the child doesn't even have to use their own money. The IRS allows a parent or grandparent to make the contribution on the child's behalf, as long as the child had the earned income to back it up.

You can find the latest numbers and rules on IRA contribution limits directly from the IRS. This small move transforms a teenager's pocket money into a cornerstone of their future wealth.

The essence of multi-generational planning is turning today's small efforts into tomorrow's significant wealth. A teenager’s summer job, paired with a parent’s intentional planning, can become a foundational asset long after today’s expenses are forgotten.

The Power of an Early Start

The biggest benefit of opening an IRA for a child is giving their money the one thing most adults wish they had more of: time. The power of compound growth over 50 or 60 years is almost unbelievable.

Let’s run the numbers. Say you help your child contribute just $2,000 a year from age 15 to 25. That’s a total of $20,000 out of pocket. Assuming a pretty standard 7% average annual return, that investment could balloon to roughly $298,000 by age 65—without them ever contributing another dime.

This isn't just about the money, though. It’s about the lessons. It teaches the value of hard work, the discipline of saving, and the long-term vision needed for "Building Wealth and Redefining the American Dream." You're not just opening an account; you're setting a precedent for a lifetime of smart financial decisions.

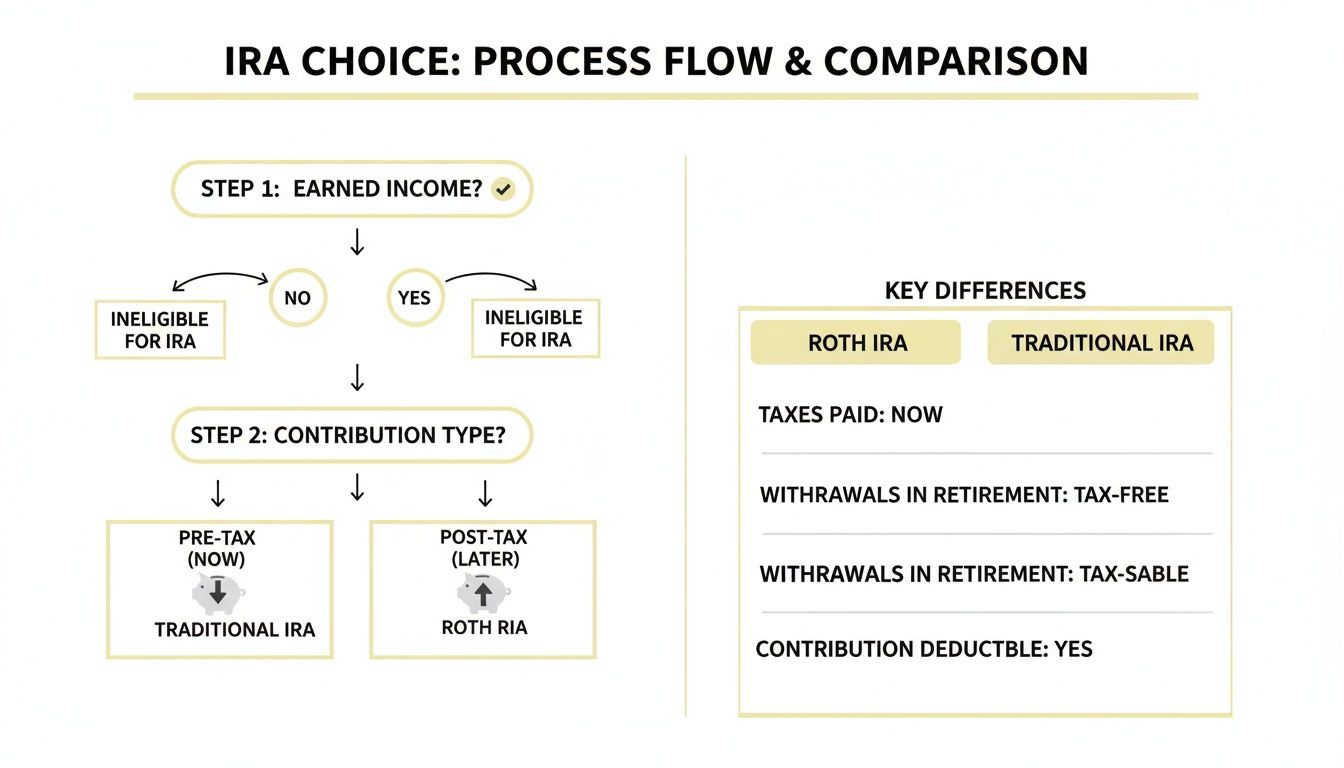

Once you've confirmed your child has earned income, the next big decision is picking the right type of retirement account. You’ll basically run into two choices for a minor: a Custodial Roth IRA or a Custodial Traditional IRA. They sound almost the same, but how they’re taxed makes a world of difference.

For a young saver, one of these is almost always the clear winner.

The whole decision really comes down to one simple question: When do you want to pay taxes? A Traditional IRA lets you potentially deduct contributions now, but every penny withdrawn in retirement gets taxed as regular income. A Roth IRA is the opposite—you contribute after-tax money, so there's no immediate tax break, but all qualified withdrawals down the road are 100% tax-free.

For a kid, that’s not just a small detail. It’s everything.

Why The Roth IRA Is a No-Brainer for Kids

Just think about your child’s financial picture right now. If you have a teenager pulling in a few thousand dollars from a summer job, their income tax bracket is probably the lowest it will ever be. In fact, they might owe $0 in federal income tax.

This is the golden ticket.

When they contribute to a Roth IRA, they pay taxes on that income today—when the tax bill is tiny or even non-existent. In exchange, every single dollar that money earns over the next 50+ years can be pulled out completely tax-free. They get decades of compound growth without ever owing the IRS another cent on it.

A Traditional IRA flips that script. You’d be skipping a tiny tax bill today only to have them pay income tax on a much, much larger pot of money decades from now, when they’re almost certainly in a higher tax bracket. It's a classic case of paying a little now to save an absolute fortune later.

A Real-World Scenario

Let's make this crystal clear. Imagine 15-year-old Maya earns $4,000 lifeguarding over the summer. Her parents help her open an IRA and contribute the full amount.

-

Path 1 (Roth IRA): Maya's $4,000 in earnings is well below the standard deduction, so she owes no federal income tax. That $4,000 goes into her Roth IRA post-tax (in this case, with a 0% tax hit). It grows for 50 years. By the time she’s 65, that account could be worth over $88,000 (assuming a 6% average annual return), and every penny is hers to keep, tax-free.

-

Path 2 (Traditional IRA): The contribution might offer a tax deduction, but since Maya owes no tax anyway, that deduction is worthless. When she’s 65, that same $88,000 is fully taxable. If she’s in a 22% tax bracket during her retirement years, she'd owe Uncle Sam nearly $20,000 in taxes.

The choice is obvious. The Roth IRA leverages a child's low-income years to create a lifetime of tax-free wealth. For a deeper dive into the mechanics and benefits, our complete guide on the custodial Roth IRA for minors breaks it all down.

By choosing a Roth IRA for your child, you are not just saving for them; you are making a strategic tax decision that will pay dividends for the rest of their life. You're locking in today's low tax rate forever.

Custodial Roth IRA vs Traditional IRA for a Child

Sometimes seeing things side-by-side makes the decision easiest. Here’s a quick comparison of how the two accounts stack up when opened for a child.

| Feature | Custodial Roth IRA | Custodial Traditional IRA |

|---|---|---|

| Tax on Contributions | Made with after-tax money. | Contributions might be tax-deductible. |

| Tax on Withdrawals | Qualified withdrawals in retirement are 100% tax-free. | Withdrawals are taxed as ordinary income in retirement. |

| Best For a Child? | Almost always. The child pays little or no tax now, locking in decades of tax-free growth. | Rarely. The immediate tax deduction is usually wasted on a low-income earner. |

| Flexibility | Contributions can be withdrawn anytime, tax-free and penalty-free (e.g., for college). | Early withdrawals generally face both taxes and penalties. |

The Roth IRA has another trick up its sleeve: flexibility. If your child ever needs to tap into the money for a big life event—like a down payment on a first home or even to help with college tuition—they can withdraw their original contributions without paying any taxes or penalties.

This incredible dual purpose makes the Roth IRA an amazingly versatile tool for a young person just starting their financial journey.

How to Open and Fund Your Child's IRA

Alright, let's move from theory to action. This is the rewarding part—where you start building real multi-generational wealth. Now that you see the incredible power of a custodial IRA, especially a Roth, let's walk through the practical steps of getting one opened and funded for your child. It's more straightforward than you might think.

The first big decision is where to open the account. You'll need a financial institution that offers custodial IRAs, which are accounts specifically designed for minors. As the custodian, you'll manage the account for your child until they reach the age of majority in your state (usually 18 or 21).

Many of the big-name brokerage firms make this incredibly easy for parents. Some popular spots include:

- Fidelity: Known for its user-friendly platform and no-fee IRAs, Fidelity offers a dedicated "Roth IRA for Kids."

- Charles Schwab: Another industry giant, Schwab provides custodial IRAs with a massive range of investment choices.

- Vanguard: Famous for its low-cost index funds, Vanguard is a fantastic choice if you're aiming for a long-term, set-it-and-forget-it strategy.

When you're comparing firms, keep an eye out for no account minimums, zero maintenance fees, and a solid selection of low-cost investments like ETFs and mutual funds.

Gathering Your Documents

Once you've picked a brokerage, the application is usually online and takes just a few minutes. To keep things moving smoothly, it really helps to have all your information ready to go before you start.

You'll need documents for both yourself (the custodian) and your child (the beneficiary). Be prepared with:

- Your full name, date of birth, and Social Security number.

- Your child’s full name, date of birth, and Social Security number.

- Your contact information, including your address and phone number.

The one non-negotiable piece of information is your child’s Social Security number. You simply cannot open an IRA without one.

This flowchart gives you a simple visual for weighing the Roth vs. Traditional IRA decision.

As you can see, the Roth IRA's tax-free growth—that upward arrow—makes it the clear winner for a young earner who is in a low (or zero) tax bracket today.

Meticulously Tracking Your Child's Income

This is the single most important part of staying on the right side of IRS rules. It's especially critical if your child's income is from informal jobs that don't issue a W-2. You absolutely must be able to prove they had legitimate earned income to justify every dollar you contribute.

Keeping clear, consistent records isn't just about following rules; it’s about treating your child’s first business venture with the respect and seriousness it deserves. It’s their first lesson in professional financial management.

Don't overcomplicate this part. A simple spreadsheet or even a dedicated notebook is all you need. For each job, just log the basics:

- Date: When was the work done?

- Service: What did they do? (e.g., "Babysitting for the Smith family," "Mowed Johnson's lawn")

- Client: Who paid them?

- Amount Paid: How much did they earn?

If they get paid through an app like Venmo or Zelle, ask the payer to add a clear note like "For babysitting 10/26." This creates a fantastic digital paper trail that backs up your logbook. This diligence is what lets you confidently answer the question, "Can I open an IRA for my child?" with a documented "yes."

Funding the Account

Once the account is open and you've got the income documented, it's time to make a contribution. A common point of confusion is whose money can actually go into the account. The good news? The IRS is wonderfully flexible here.

The contribution does not have to come from the money the child actually earned. As long as they have the earned income on the books for that year, anyone—a parent, grandparent, or other loved one—can contribute on their behalf. This is an absolutely fantastic way to give a gift with a lifelong impact.

For example, let's say your daughter earns $1,500 from her summer job and spends it all on clothes and movies. You can still contribute $1,500 of your own money into her Roth IRA as a gift. This strategy, sometimes called a "family match," teaches the immense value of saving without forcing a teenager to give up all their hard-earned cash.

For a deeper dive into these kinds of strategies, our guide to the Roth IRA for kids offers more practical tips. By following these steps, you'll successfully turn your child's first job into a powerful engine for building wealth that can last a lifetime.

Smart Strategies for a Child's IRA

Opening the account is a fantastic first step, but the real magic happens next. This is where you transform a simple savings vehicle into a hands-on workshop for financial discipline, long-term thinking, and even legacy building. It’s about making the IRA a living, breathing part of your family's financial story.

The strategies that follow are more than just clever funding mechanisms. They’re conversation starters that teach invaluable lessons about work, saving, and the incredible power of time.

The Power of the Family Match

One of the most effective strategies I've seen is the "family match." The concept is simple: for every dollar your child earns and agrees to put in their IRA, you match it with a contribution of your own. This turns a parental gift into a powerful incentive.

Think about it from their perspective. If your 16-year-old earns $2,000 from a summer job, the temptation to spend it on a car or clothes is huge. But if you offer to put $2,000 of your own money into their IRA if they commit their earnings, the deal becomes much sweeter.

Suddenly, they get the satisfaction of seeing $4,000 go to work for their future, funded by their own hard work and your support.

This approach does a few important things all at once:

- It directly links their work to long-term savings.

- It doubles the impact of their efforts, making saving feel way more rewarding.

- It teaches the concept of an employer match (like in a 401(k)) years before they ever enter the corporate world.

The family match sends a clear message: We believe in your hard work, and we’re willing to invest right alongside you.

Turning Gifts into a Lasting Legacy

Grandparents are always looking for meaningful ways to give gifts that last longer than the latest gadget. Contributing to a grandchild's IRA is a perfect fit, but you have to do it correctly. Remember, the child must have earned income to cover the total contribution amount.

Here’s how it works in practice. Let's say your son earned $1,000 from his weekend job mowing lawns. For his birthday, his grandparents can gift him $1,000 by contributing it directly to his Custodial IRA. The gift is made on behalf of the child, backed by the income he already earned.

This strategy transforms a traditional birthday check into a seed for multi-generational wealth. It’s a gift that says, "I'm not just thinking of you today; I'm investing in the person you will become 50 years from now."

This is a fantastic way for the entire family to get involved in building the child's financial foundation. It shifts the focus of gifting from temporary consumption to permanent security.

Demystifying Investing for Young Minds

Once the money is in the account, what do you do with it? This can feel intimidating, but for a child's IRA with a 50+ year time horizon, the best strategy is often the simplest one. You don't need to be a stock-picking genius.

The goal is to choose investments that are diversified, low-cost, and easy to understand. This is where low-cost index funds or exchange-traded funds (ETFs) are absolute heroes.

Think of an S&P 500 index fund as buying a tiny slice of 500 of America's largest companies. Instead of betting on one company to succeed, you're betting on the long-term growth of the U.S. economy as a whole. It’s a straightforward and historically proven way to build wealth over time.

By explaining this concept to your child, you're demystifying the stock market. You're showing them that investing isn't about gambling; it's about ownership and patient participation in economic growth. This is a foundational lesson for "Building Wealth and Redefining the American Dream."

While the IRA is primarily a retirement tool, a Roth IRA’s flexibility also makes it a potential backup for education costs. For a detailed breakdown of how it stacks up against other options, exploring a 529 vs Roth IRA comparison can bring a lot of clarity to your family's goals.

Ultimately, these strategies are about more than just numbers on a statement. They're about instilling a mindset. When you open an IRA for your child, you're giving them a front-row seat to the most powerful wealth-building tool on the planet: compound growth fueled by time.

A Glimpse Into the Future of Kids’ Retirement Accounts

While custodial IRAs are an incredible tool today, the rules of the game are always changing. There’s a pretty significant development on the horizon that could completely reshape how families save for their children's futures—even for kids without a single dollar of earned income. If you're serious about family financial planning, it pays to know what’s coming down the pipeline.

Starting in 2026, the landscape for kids’ retirement savings is set to get a lot more interesting. A new type of IRA, nicknamed the “Trump Account,” is expected to launch for children in the U.S. under the One Big Beautiful Bill Act. If it goes live as planned, any child under 18 with a Social Security number can have one opened for them. This is a monumental shift from the rules we follow today. You can get more of the nitty-gritty details on these new tax-advantaged savings accounts from natlawreview.com.

A New Era for Childhood Savings

The single most striking feature of these proposed accounts is the total elimination of the earned income requirement. Let that sink in. This is a true game-changer. It means you could open an IRA for a child from the day they're born, whether they’re mowing lawns or just learning to crawl.

Under the proposal, parents, grandparents, and other family members could contribute up to $5,000 each year. This limit is completely separate from the regular IRA contribution limits for adults, carving out a dedicated savings lane for the next generation. It’s a powerful way for families to start building a nest egg from day one.

These accounts also come with a special “growth period,” which locks the funds in until the year the child turns 18. This feature is designed to protect the savings and force them to benefit from decades of compounding, free from the temptation of early withdrawals.

Unique Ways to Fund and Supercharge the Account

Trump Accounts are also slated to introduce some really unique funding mechanisms that set them apart from any custodial IRA we've seen before.

- Federal Seed Money: A federal pilot program is designed to seed accounts for children born between January 1, 2025, and December 31, 2028, with a $1,000 government deposit. This initial boost wouldn't even count toward the annual $5,000 contribution cap.

- Employer Contributions: Employers would be able to contribute up to $2,500 per year to an employee's dependent’s Trump Account. And, crucially, these contributions would not be considered taxable income to the employee.

This creates a powerful stacking opportunity. Between personal contributions, an employer match, and the federal seed money, a child could see a huge amount invested for them each year.

Just imagine this for a second: a family contributes the full $5,000, their employer kicks in another $2,500, and the government seeds the account with $1,000. That’s an $8,500 infusion into a tax-advantaged account in a single year for a toddler, setting an incredible foundation for their financial future.

This forward-thinking account adds a new, rules-based way to align a child’s early years with long-term financial security. For families dedicated to “Building Wealth and Redefining the American Dream,” understanding these future options is the key to making the smartest financial moves possible.

Got Questions About Your Kid’s IRA?

Once you start thinking about opening an IRA for your child, the "what ifs" tend to pop up. It’s only natural. You'll start wondering how this whole thing works in the real world, especially as your kid grows up. Getting a handle on these common questions is the key to moving forward with confidence.

These accounts are designed to grow with your child, eventually becoming their own. Understanding that journey helps you frame the conversation about financial responsibility from day one.

What Happens When My Child Becomes an Adult?

This is the big one. The moment your child hits the age of majority in your state—that's usually 18 or 21—your job as the custodian is officially over. The account automatically becomes theirs, free and clear.

From that day on, it's just a regular individual retirement account in their name. They can change the investments, decide how much to contribute, or take money out according to the standard IRA rules. This transition is exactly why teaching them about money early is so critical. You're not just building them a nest egg; you're preparing them to manage it wisely.

Does a Custodial IRA Hurt College Financial Aid?

This is a huge source of anxiety for parents. Will a savings account in my child's name tank their chances for college financial aid? Here's the good news: while a custodial IRA is legally your child's asset, its impact on the FAFSA (Free Application for Federal Student Aid) is usually minimal.

Retirement assets, including Roth and Traditional IRAs, are generally not counted as reportable assets when calculating the Student Aid Index. This means the account balance itself typically doesn't hurt their eligibility for financial aid.

The long-term advantage of decades of tax-free growth typically far outweighs any potential, minor impact on financial aid calculations. It's a strategic trade-off for their future financial freedom.

Can My Child Use IRA Money for College?

Yes, they can! This is where a Roth IRA, in particular, becomes an incredibly flexible tool. Think of it as a hybrid account for both retirement and education.

Here’s the breakdown:

- Contributions: Your child can pull out their direct contributions—the actual cash you or they put in—anytime, for any reason, without paying taxes or penalties. This makes it a fantastic backup fund for unexpected college costs.

- Earnings: They can also withdraw the investment earnings to pay for qualified education expenses without the usual 10% early withdrawal penalty. They will, however, owe regular income tax on that growth.

How Do I Prove My Child's Income Without a W-2?

This is a fantastic question, especially for kids earning cash from side hustles like babysitting, mowing lawns, or lifeguarding. The IRS definitely requires proof of legitimate earned income, but a W-2 is not the only way to do it.

The secret is simple: diligent record-keeping. A basic spreadsheet or even a notebook is your best friend here. For every gig, you need to log:

- The date the work was done.

- A quick description of the job (e.g., "Mowed the Miller's lawn").

- Who paid them.

- The exact amount they were paid.

Keeping records of digital payments, like Venmo transactions with clear notes in the memo line, also creates a perfect paper trail. This documentation keeps you compliant with the rules while giving your child a massive head start on their financial future.

At Smart Financial Lifestyle, we believe in making smart financial decisions that build a lasting legacy. For more insights on multi-generational wealth, explore our resources at https://smartfinancialifestyle.com.