Maximize Your Estate: what is a living trust vs will for Your Assets

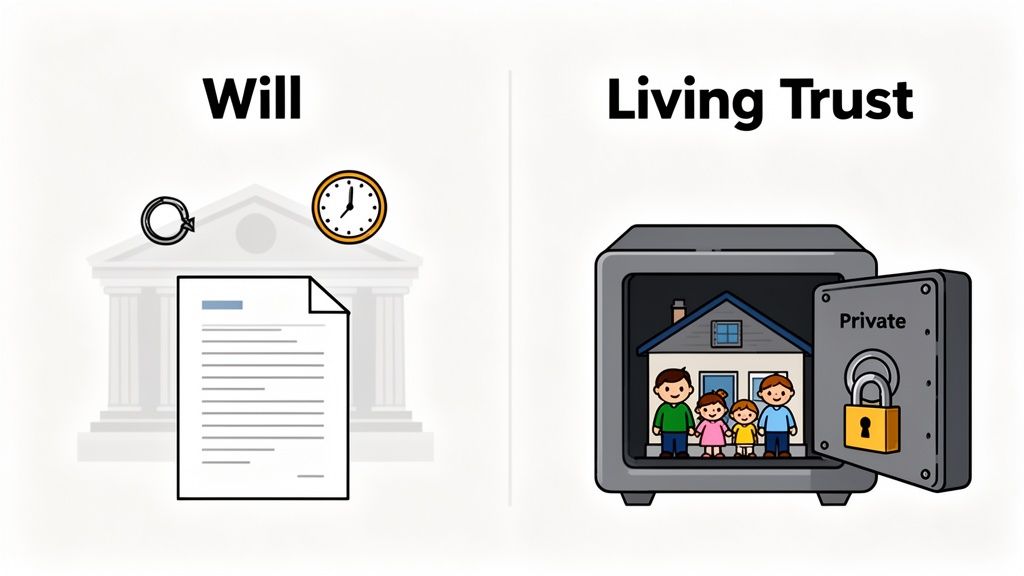

At its core, the difference between a living trust and a will boils down to one critical process: probate. A will is simply a set of instructions for what happens after you die. Because of that, it has to go through the public court process of probate. A living trust, on the other hand, is a private entity you create to hold and manage your assets during your life and after your death, skipping probate entirely.

Living Trust vs Will Key Differences at a Glance

Choosing the right estate planning tool can feel overwhelming, but when you understand the core purpose of each, the decision gets a whole lot clearer. A Last Will and Testament is the foundational document that spells out your final wishes. It names an executor to handle things and, crucially, appoints guardians for your kids. It's straightforward, but it also opens your estate up to public view and potential delays in probate court.

A revocable living trust, however, is a much more dynamic tool. You're essentially creating a separate legal entity and then transferring ownership of your assets—like your home, investments, and bank accounts—into it. The best part? You stay in complete control as the trustee while you're alive. When you pass away, the successor trustee you've chosen takes over and distributes everything according to your private instructions, avoiding the time and cost of probate. This single difference has a massive impact on your family's experience after you're gone.

Core Differences Between a Will and a Living Trust

This table offers a clear, high-level summary of how a will and a living trust function, helping you quickly understand the most critical distinctions.

| Feature | Last Will and Testament | Revocable Living Trust |

|---|---|---|

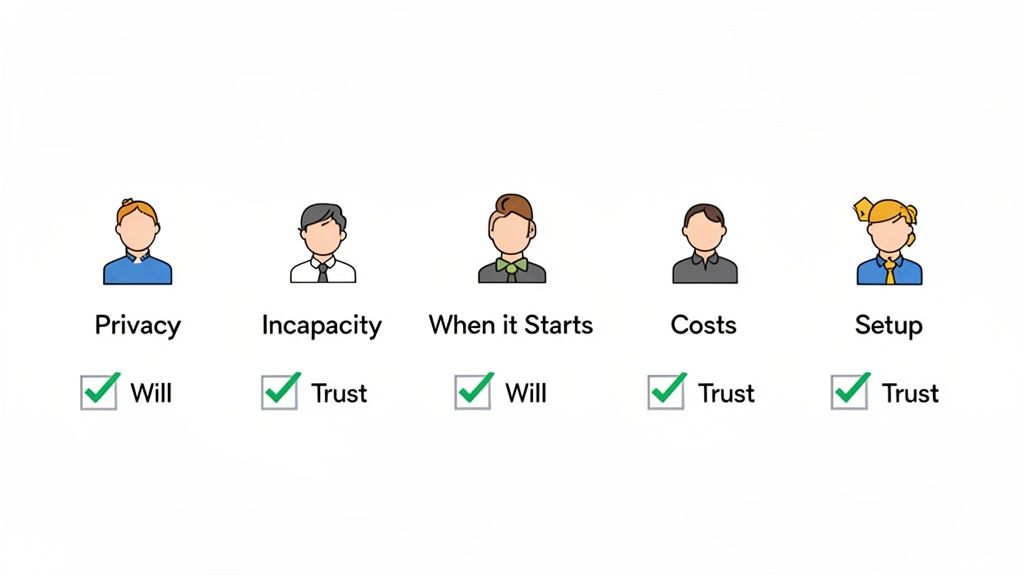

| When it Takes Effect | Only upon your death. | Immediately upon creation and funding. |

| Probate | Required. Assets go through court. | Avoids probate for all trust assets. |

| Privacy | Becomes a public court record. | Remains a private document. |

| Incapacity Plan | No protection; may require conservatorship. | Successor trustee manages assets if you can't. |

| Upfront Cost | Lower initial cost to create. | Higher initial cost to create and fund. |

The primary reason families choose a living trust is to shield their loved ones from the complexities and publicity of the probate process, ensuring a smooth and private transition of wealth.

Unfortunately, a staggering 55% of Americans don't have any estate planning documents in place whatsoever. That means the vast majority of families are leaving their financial futures to chance, which can create incredible, unnecessary stress for their loved ones.

Understanding how each of these tools works is the first step toward making a smart decision for your legacy. For a deeper look into how this entity works, you can check out our guide on what is a revocable living trust.

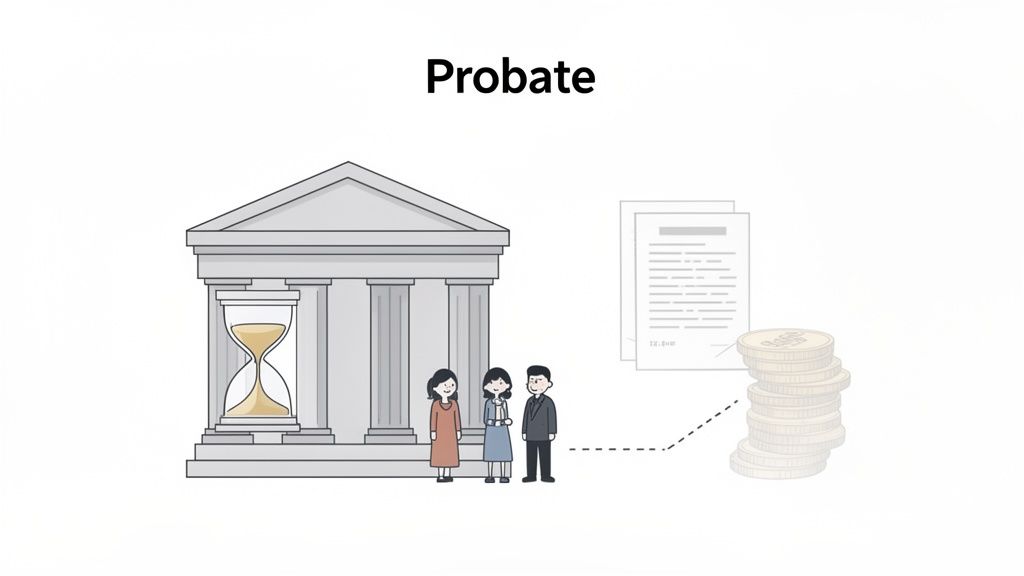

How Probate Shapes Your Estate Planning Decision

To really get the difference between a living trust and a will, you first have to understand probate. Probate is the formal court process that kicks in after you pass away to validate your will, pay off your final debts, and legally transfer your assets to your loved ones. While it sounds like a simple administrative step, probate is often a major source of stress, cost, and long delays for grieving families.

When an estate goes through probate, the will becomes a public document. Every single detail—from the assets you owned to who gets what—is filed with the court and becomes accessible to anyone who cares to look. For families who value their privacy, this public airing of their financial life can be deeply uncomfortable.

Beyond the lack of privacy, the process itself can drag on for what feels like an eternity. The exact timeline depends on your state and how complex the estate is, but it's not unusual for probate to last anywhere from several months to well over a year. During this entire time, your assets are essentially frozen, meaning your beneficiaries can't access their inheritance until the court finally gives the green light.

The Financial Toll of Probate

What often shocks families the most are the costs that come with probate. These expenses get paid directly out of the estate’s assets, which means the inheritance you wanted your loved ones to have gets smaller before they ever see a dime.

These costs usually include things like:

- Court Filing Fees: Every estate has to pay fees just to get the probate case started and processed.

- Attorney Fees: An executor almost always needs a lawyer to help them through the legal maze, and those fees can be significant.

- Executor Compensation: The person you named as your executor is entitled to a fee for their time and effort, usually set by state law or the will itself.

- Appraisal and Valuation Fees: The court requires formal appraisals of assets like real estate, vehicles, and business interests to determine their value.

For many families, these costs can easily eat up 3% to 8% of the total estate value. Think about that. On a $500,000 estate, you could lose between $15,000 and $40,000 just to the probate process—money that should have gone straight to your heirs. Our detailed guide on how to avoid probate court breaks down strategies to shield your assets from these hefty reductions.

How a Living Trust Bypasses This Process

This is where the power of a living trust really shines. A trust is a private legal entity that holds title to your assets. Because you already transferred ownership of your property into the trust while you're alive, there’s nothing for the court to oversee when you're gone. The assets simply aren't part of your "probate estate."

Instead of a public court case, your successor trustee—the person you chose to take over—simply follows the private instructions you left in the trust document. They can pay any final bills and distribute the assets directly to your beneficiaries without court approval, frustrating delays, or public prying.

"The single most compelling reason to use a living trust is to avoid probate. It’s a strategic choice to ensure your family receives their inheritance efficiently and privately, preserving both the value of your estate and their peace of mind during a difficult time."

Let's look at how this plays out for two different families in a real-world scenario.

Scenario A: The Will

John passes away with a will, leaving his $700,000 estate—including a house and an investment portfolio—to his two children. His will has to be filed with the probate court. His kids end up waiting 14 months for the court process to finish, paying over $25,000 from the estate in legal fees, executor compensation, and court costs.

Scenario B: The Living Trust

Sarah passes away with a properly funded living trust that holds her identical $700,000 estate. Her daughter, acting as the successor trustee, pays the final expenses and distributes all the assets to herself and her brother within just six weeks. The entire process is private, and the only costs are for preparing a final tax return and some minor administrative tasks, saving the family more than $20,000 and a full year of waiting.

This stark difference is why understanding probate is absolutely critical when you're deciding between a will and a trust.

A Detailed Comparison of Core Features

To really get to the heart of the living trust vs. will debate, we have to look past the definitions and see how they actually perform in the real world. This isn't about which one is "better" in a vacuum. It's about figuring out which one better serves your family’s specific needs when it comes to privacy, control, and costs. Let's put them side-by-side to see where they shine.

Privacy: Public Records vs. Private Documents

One of the biggest differences is privacy. When a will goes through probate, it becomes a public court record. That means anyone—from a nosy neighbor to a predatory salesperson—can look up a full inventory of your assets, their value, and exactly who got what.

A living trust, on the other hand, is a completely private document. Its administration happens outside the court system, keeping your family’s financial business shielded from public eyes. For many people, this alone makes a trust the clear winner.

Living trusts offer three critical advantages that fundamentally change how your family experiences your legacy. First, privacy is paramount. When you establish a will, it becomes a public record once filed with the court... Living trusts, by contrast, remain private documents that shield all details of your estate from public scrutiny. Discover more insights on how trusts protect your family's information from public access on johnhancock.com.

Control During Incapacity

What happens if you get sick or injured and can't manage your own affairs? This is where the distinction between a will and a trust becomes crystal clear. A will only kicks in after you die, so it offers zero protection for incapacity.

If you only have a will, your family would likely have to go to court to get a conservatorship or guardianship. This is a public, expensive, and often emotionally draining legal process where a judge appoints someone to take over your finances.

A living trust is built for this exact scenario. Your trust document names a successor trustee who can step in immediately and privately to manage your assets if you become incapacitated. This smooth transition of control avoids court, saving your family time, money, and stress when they can least afford it.

When They Take Effect

This difference is simple but has massive implications.

- A Will: Only becomes active the day you die. Think of it as a letter of instruction to the probate court.

- A Living Trust: Becomes active the moment you sign it and fund it. It’s a living, breathing document that manages your assets during your life, through incapacity, and after your death.

A trust gives you lifetime benefits—especially for asset management and incapacity planning—while a will is purely an after-death tool.

To help you visualize how these differences play out, here’s a quick table breaking down common family situations and how each document handles them.

Scenario-Based Comparison: Will vs. Living Trust

This table provides a detailed, point-by-point comparison across key legal and practical dimensions to help you evaluate which option fits your situation.

| Consideration | Last Will and Testament | Revocable Living Trust |

|---|---|---|

| Probate | Assets must go through the public, often lengthy, and costly probate court process. | Properly funded assets completely bypass probate, allowing for a private and efficient transfer. |

| Privacy | Becomes a public record upon death, exposing your assets, heirs, and distributions to anyone. | Remains a private document, shielding all financial details from public view and protecting your family’s privacy. |

| Incapacity Planning | Offers no protection. A separate Power of Attorney is needed, or the court may need to appoint a conservator. | Names a successor trustee to manage your affairs seamlessly if you become incapacitated, avoiding court intervention. |

| Effective Date | Only takes effect after your death. | Takes effect as soon as it is signed and funded, providing benefits during your lifetime. |

| Upfront Cost | Generally lower initial cost to draft and sign. | Higher initial cost due to its complexity and the need to fund it by retitling assets. |

| Long-Term Cost | Can be very expensive in the long run due to probate fees, which can consume 3% to 8% of the estate's value. | Often saves significant money long-term by avoiding probate costs, making the upfront investment worthwhile. |

| Asset Control | You control assets directly until death. After death, the court-supervised executor takes over. | You control assets as the trustee during your lifetime. Your successor trustee takes over upon incapacity or death without court. |

| Minor Children | Can name a guardian, but any inheritance for them is controlled by the court until they turn 18. | Can create sub-trusts to hold and manage a child’s inheritance, specifying when and how they receive it (e.g., at age 25 or 30). |

| Special Needs Heirs | A direct inheritance can disqualify a special needs heir from receiving crucial government benefits. | Can create a Special Needs Trust to provide for the heir without jeopardizing their eligibility for benefits. |

| Out-of-State Property | Requires a separate probate process ("ancillary probate") in each state where you own real estate, adding cost and delay. | Avoids ancillary probate entirely, as the trust owns the property, not you. |

As you can see, the choice isn't just about avoiding probate. It's about maintaining control, protecting your family's privacy, and planning for life's uncertainties.

Overall Costs: Upfront vs. Long-Term

When we talk about money, you have to look at the whole picture. A will is almost always cheaper to create upfront. But its true cost comes later during probate, where court fees, attorney costs, and executor payments can chip away at your estate by 3% to 8%.

A living trust costs more to set up because it’s a more detailed legal document, and you have the extra step of "funding" it by retitling assets. While that initial investment is bigger, a well-funded trust avoids the probate process entirely, often saving your family tens of thousands of dollars down the road. It’s a classic case of paying more now to save a lot more later.

Setup and Maintenance

Creating a will is fairly simple. You meet with an attorney, sign the document with witnesses, and stick it in a safe place. There’s not much to do after that besides reviewing it every few years or after a major life event.

Setting up a living trust takes more effort. After creating the trust document, you have to actively transfer ownership of your major assets—your house, bank accounts, brokerage accounts—into the name of the trust. This is called funding the trust, and it's a critical step. An unfunded trust is a common and costly mistake, as any assets left out of it will probably still end up in probate.

It’s also crucial to remember that some assets, like retirement accounts and life insurance, pass to your loved ones through beneficiary designations, not your will or trust. You can learn more about how this works by checking out our guide on what is a beneficiary designation. Making sure those designations align with your overall plan is a key piece of the puzzle.

Analyzing the True Cost of Estate Planning

When you stack up a living trust vs. a will, one of the first things that jumps out is the price tag. It’s easy to look at the initial setup fees and think a will is the clear winner for your wallet. But that’s only looking at half the picture. The real cost of an estate plan isn’t just what you pay an attorney today, but what your family will end up paying down the road.

A will is almost always cheaper to get started. The legal work is more straightforward, and the whole process is pretty quick. That low barrier to entry makes it a popular choice for a lot of people.

However, the true financial punch of a will lands after you’re gone. Because a will has to go through probate, your estate gets hit with a whole range of backend costs that can take a serious bite out of the inheritance you leave behind. And the kicker? Those expenses get paid right out of your estate’s assets before your loved ones see a dime.

The Upfront Investment in a Trust

Creating a living trust definitely requires a bigger investment upfront. That's because a trust is a more sophisticated legal tool designed to manage your assets both during your life and after you pass. The higher fee isn't just for drafting the document itself; it covers the most important part: funding the trust.

Funding is the process of legally retitling your major assets—think your house, brokerage accounts, and bank accounts—into the name of the trust. It’s a meticulous, administrative process that takes time and effort, which is why it costs more. But this is the very step that lets your estate completely sidestep probate later.

Think of a living trust as a pre-paid express pass for your estate. You’re paying more now so your family can skip the long, expensive, and stressful lines at the probate court system later.

Unpacking the Hidden Costs of a Will

While a will looks like a bargain at first, its journey through probate court introduces a bunch of costs that can pile up fast. Getting a handle on these potential expenses is the key to making a truly smart financial decision for your family.

The most common costs that pop up during probate include:

- Court Filing Fees: Every probate case has fees just to get the case opened and managed by the court system.

- Executor Compensation: The executor you name is legally entitled to get paid for their work, which is often calculated as a percentage of the estate's total value.

- Legal Fees: Most executors need to hire an attorney to help them navigate the probate maze. These legal fees can be one of the biggest expenses, sometimes also based on a percentage of the estate.

- Appraisal and Business Valuation Fees: The court needs formal appraisals of real estate and other major assets to figure out their exact value for the public record.

Setting up a living trust can run anywhere from $1,000 to $10,000 or more, depending on how complex your situation is. By comparison, you could get a basic will drafted for just $150 to $1,000. But once that will hits probate, the fees can easily eat up 3% to 8% of your estate's total value, making those initial savings look tiny. You can get a deeper dive into these financial realities in this detailed overview from BestLawyers.com.

A Financial Model for Your Legacy

Let's run the numbers with a real-world example to see how this actually plays out.

Imagine an estate valued at $800,000.

- With a Will: Let's say probate costs average out to 5% of the estate's value. That comes out to a whopping $40,000. This money is pulled directly from the inheritance.

- With a Living Trust: The family might have paid $4,000 to have the trust properly set up and funded. By avoiding probate, they save the estate that $40,000 expense, which means a net savings of $36,000.

This simple breakdown shows that the higher upfront cost of a trust isn’t really an expense at all—it’s a strategic investment in protecting your family’s inheritance. It completely changes the question from "Which is cheaper to create?" to "Which one will preserve more of my hard-earned wealth for the people I love?"

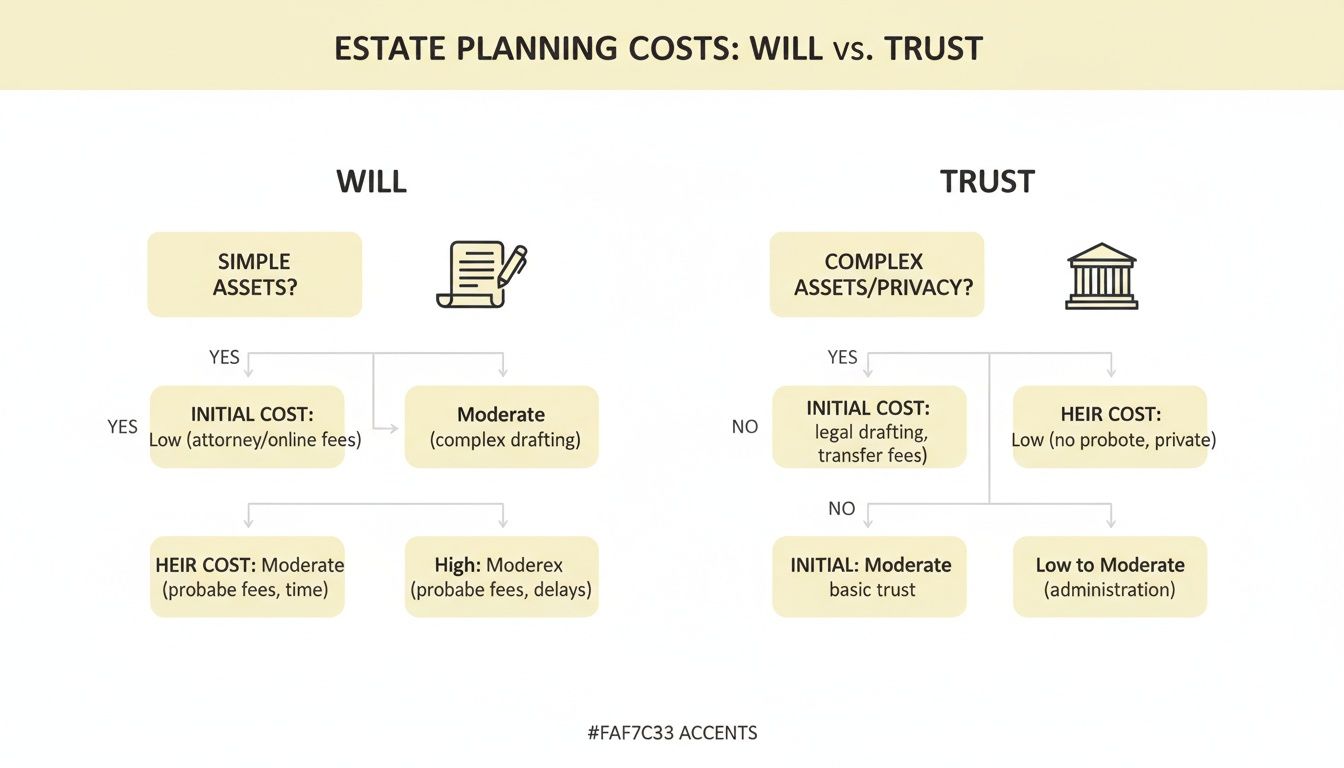

Which Is Right for Your Family's Situation?

Deciding between a will and a trust isn't about finding a single "best" answer. It's about finding the right fit for your unique life circumstances. The choice really hinges on how complex your finances are, your family dynamics, and what you want for the future. By looking at a few common scenarios, you can start to see which tool makes the most sense for the legacy you want to leave.

A big piece of this is understanding the financial trade-offs, which this decision tree on estate planning costs makes crystal clear.

As you can see, a will costs less to set up. But a trust is built to slash the long-term financial burden on your heirs by keeping them out of probate court.

When a Will Is Often the Right Choice

For many people, especially those just starting to build their wealth, a will provides crucial protection without getting overly complicated. It’s the foundational document every adult should have, especially if there are minor children in the picture.

A will is usually the most practical and sufficient choice if you are:

- A Young Individual or Couple with Limited Assets: If you don't own real estate and your assets are below your state's probate threshold, a will gets the job done. It will effectively distribute your property and—most importantly—name guardians for your children.

- Someone Prioritizing Simplicity and Low Upfront Costs: Wills are straightforward and much less expensive to create. They accomplish the primary goal: directing where your assets should go when you're gone.

A will is the only legal document where you can name a guardian for your minor children. If you have kids, this function alone makes a will absolutely non-negotiable, regardless of whether you also have a trust.

When a Living Trust Becomes Essential

As your life and finances grow, the limitations of a simple will become more obvious. This is where a living trust steps in, offering far more control, privacy, and protection for your assets and family.

Think of a living trust as the superior option in these common situations:

- You Own Real Estate: If you own a home, a trust is almost always the recommended tool. Transferring your home into a trust ensures it passes directly to your beneficiaries without getting stuck in the probate process, which can be painfully long and expensive for real estate.

- Your Assets Exceed Probate Limits: Every state sets a threshold for what it considers a "small estate." If your assets are valued above that limit, probate is mandatory. A trust allows you to bypass this requirement entirely.

- You Want to Plan for Incapacity: A will does nothing for you if you become unable to manage your own affairs. A trust, on the other hand, allows your chosen successor trustee to step in and manage your finances seamlessly—no court intervention needed.

- You Have a Blended Family: Trusts provide incredible control for directing assets in blended family situations. You can ensure your current spouse is cared for during their lifetime while guaranteeing your assets ultimately go to your children from a previous relationship.

- You Value Privacy: If keeping your financial affairs out of the public record is a priority, a trust is the only way to go. It's a private document, unlike a will, which becomes public during probate.

The Power of Using Both Together

Here's a secret the pros know: the most effective estate plan often isn't an "either/or" choice. For many families, the smartest strategy is to use a living trust as the primary tool for asset transfer and a special type of will, called a pour-over will, as a safety net.

This combination creates a powerful, two-part system:

- The Living Trust: This holds and manages your major assets (your home, investments, etc.). It allows them to bypass probate for a quick, private, and cost-effective distribution to your heirs.

- The Pour-Over Will: This will has one main job—it "pours" any assets accidentally left out of the trust into the trust when you pass away. It also serves as the official document where you name guardians for your minor children.

This integrated approach gives you the best of both worlds. You get the probate-avoidance and incapacity-planning benefits of a trust, plus the essential guardianship-naming function of a will. It ensures all your bases are covered, creating a truly secure plan for your family's future.

Taking the Next Step to Lock In Your Legacy

Figuring out the difference between a living trust and a will is a great start, but that knowledge only becomes powerful when you use it. I know that moving from learning to actually doing can feel like a huge leap, but you can tackle it with a clear, step-by-step plan. Think of this as your roadmap to get your thoughts organized before you sit down with a pro, making sure you build a legacy that truly reflects what you care about and protects the people you love.

Start with a Personal Asset Inventory

Before you can decide how to pass things on, you have to know exactly what you own. This isn’t just some homework assignment for your attorney; it’s a powerful way for you to get crystal clear on your financial picture.

Just create a simple, confidential list that covers all the bases:

- Real Estate: Your main home, any vacation spots, or rental properties.

- Financial Accounts: All your checking, savings, and brokerage accounts, plus any CDs.

- Retirement Savings: Your 401(k)s, IRAs, and any pension plans.

- Life Insurance Policies: Just jot down the company and the death benefit.

- Valuable Personal Property: Think cars, jewelry, art, or any family heirlooms that have significant financial or sentimental value.

- Business Interests: Any piece of a private company you own.

This list is the absolute foundation of your estate plan. It’s what you and your advisor will use to make the smartest decisions.

Define What "Legacy" Means to You

Once you've got a handle on what you have, the real question is: what do you want it all to accomplish? This goes way beyond just deciding who gets what. It’s about the story your plan will tell long after you're gone.

An estate plan is one of the most profound forms of communication you'll ever create. It’s your final opportunity to express your values, protect your loved ones, and support the causes you believe in. Taking the time to define your goals ensures that this message is clear, intentional, and impactful.

Take a minute to think about your main goals. Is it all about making sure your kids are financially secure? Or maybe you need to protect an inheritance for a loved one with special needs. Perhaps you're in a blended family and want to provide for your current spouse while making sure your kids from a previous marriage are also taken care of. You might even want to leave a lasting gift to a charity that’s close to your heart. Whatever your goals are, write them down.

Find the Right Professional for the Job

Choosing the right estate planning attorney is a huge deal. You’re not just hiring someone to fill out forms; you're looking for a trusted advisor who can wrap their head around your family’s unique dynamics and financial situation. My advice? Look for someone who specializes in estate planning—not a generalist. Ask friends for referrals, or check with your local bar association for a list of qualified attorneys.

Before you sign anything, schedule an initial consultation. This is your chance to interview them, ask the tough questions, and see if you actually click.

Checklist of Questions for Your Advisor:

- What percentage of your practice is dedicated to estate planning?

- Do you charge a flat fee or an hourly rate for creating a will or a trust?

- How do you help clients with the process of funding a living trust? Is that service included in your fee?

- What's your process for reviewing and updating plans as my life changes?

- Based on what I've told you about my goals, what challenges do you see on the horizon for my plan?

Common Questions About Wills and Trusts

Once you start digging into the details of a living trust versus a will, a few key questions always seem to pop up. Getting straight answers to these common sticking points is the best way to make a confident choice that truly protects your family.

Do I Still Need a Will If I Have a Living Trust?

Yes, absolutely. Think of a special type of will, called a pour-over will, as a critical safety net for your trust. Its main job is to "pour" any assets you might have forgotten to put in your trust's name into the trust when you die.

Besides that, a will is the only legal document where you can name guardians for your minor children. If you have kids, this makes a will an indispensable part of your plan.

Can I Make Changes to My Living Trust or Will?

Of course. So long as you are mentally competent, you can amend or completely revoke a revocable living trust whenever you want. You can also update a will with a legal amendment called a "codicil," though it's often simpler just to draft a new one to replace the old version.

It's a smart practice to review your entire estate plan every three to five years. You should also pull it out after any major life event, like a marriage, divorce, the birth of a child, or a big change in your financial situation.

What Happens If I Own Property in Multiple States?

This is a situation where a living trust really shines. If you only have a will, your family will likely face a separate, expensive, and time-consuming probate process in each state where you own real estate. This headache is known as ancillary probate.

By placing all of your out-of-state properties into a single living trust, you sidestep those multiple court proceedings entirely. It streamlines the whole process for your heirs, saving them an incredible amount of money, time, and administrative hassle.

At Smart Financial Lifestyle, we believe in making smart financial decisions that secure your family’s legacy. Our resources are designed to give you the clarity and confidence to build a plan that lasts for generations. Learn more by visiting https://smartfinancialifestyle.com.