Calculate Liquid Net Worth: A Practical Guide to Your Finances

Figuring out your liquid net worth is pretty straightforward. You just take your liquid assets (cash and stuff you can sell fast) and subtract your short-term liabilities, like credit card debt. That simple math gives you a number that reveals your immediate financial flexibility—it's one of the most important health checks for your finances.

Why Your Liquid Net Worth Is a Critical Health Check

Before we jump into the numbers, it’s really important to grasp what your liquid net worth actually means. It's so much more than just a figure on a spreadsheet. Think of it as a real-world measure of your financial security and your ability to pivot on a dime. I like to call it the family's financial first-aid kit, always stocked and ready for whatever life throws your way.

This one number is a vital tool for making smart financial moves. Whether you're juggling the complex needs of a multigenerational household, going through a major life event like a divorce or retirement, or trying to plan a meaningful legacy, knowing your liquidity is absolutely essential.

A Measure of Readiness, Not Just Riches

Your total net worth shows you what you own, but your liquid net worth tells you what you can actually use right now. That distinction is everything. Why? Because illiquid assets, like your house or a business, can't pay for an unexpected medical bill or let you jump on a last-minute investment opportunity. Those things require cash, and fast.

In my experience, the families who weather financial storms the best aren't always the ones with the highest total net worth. They're the ones with the strongest liquidity. It's that financial cushion that delivers true peace of mind.

This idea is central to making sure your wealth sends a message of stability and wisdom for generations to come.

Building a Foundation for Financial Control

Calculating this figure isn't about getting a score or seeing how you stack up against others. It's the first real step toward gaining genuine control over your financial life. Knowing this number empowers you to answer critical questions with confidence:

- Emergency Preparedness: Do we have enough cash on hand to cover at least six months of living expenses if one of us loses a job?

- Opportunity Seizing: Could we act quickly on a unique investment or business idea without being forced to sell long-term assets at a terrible time?

- Legacy Planning: Are our finances set up to provide for our loved ones without leaving them a mess of illiquid assets they can't manage?

While comparing your numbers to others can give you some helpful context (you can learn more about the net worth by age percentile in our detailed guide), the real goal here is personal. This calculation allows you to build a resilient financial foundation, turning abstract wealth into practical, everyday security.

Getting Your Arms Around Your Liquid Assets and Liabilities

To really get a handle on your liquid net worth, you first need to lay all your financial cards on the table. This means taking a clear, honest inventory of what you own that can be turned into cash in a pinch (liquid assets) and what you owe right now (liabilities). This isn't about judging past decisions—it's all about getting clarity for the road ahead.

Think of it like this: before you map out a cross-country road trip, you need to know what's in your glove box and trunk, not what’s packed away in long-term storage.

Defining Your Liquid Assets

A liquid asset is simply anything you own that can be converted into cash fast—usually within a few days—without taking a major hit on its value. The key words here are speed and accessibility.

Here are some of the most common liquid assets you'll want to list:

- Cash on Hand: It doesn’t get more liquid than the bills in your wallet.

- Checking and Savings Accounts: This is money in the bank you can get your hands on immediately.

- Money Market Accounts: These are just as accessible as savings accounts but often pay a little more interest.

- Certificates of Deposit (CDs): Even with potential penalties for early withdrawal, they're generally considered liquid because you can access the cash if you really need to.

- Publicly Traded Stocks, Bonds, and Mutual Funds: You can usually sell these within a couple of business days. If you want to dive deeper into how these are held, check out our guide on what is a taxable account.

Now, it’s just as important to know what isn't a liquid asset. Illiquid assets are valuable, sure, but you can't sell them overnight. This category includes things like your primary home, any rental properties, ownership in a private business, or collectibles like art and classic cars. These are absolutely crucial for your total net worth, but we set them aside when calculating your liquid net worth.

The real measure of your financial flexibility isn't the appraised value of your home; it's the amount of cash you could access by next Tuesday without causing a financial fire sale.

To help you sort this out, here's a quick cheat sheet for classifying your assets.

A Quick Guide to Liquid vs Illiquid Assets

Use this clear comparison to correctly categorize your assets before calculating your liquid net worth.

| Asset Category | Liquid (Easily Converts to Cash) | Illiquid (Harder to Convert to Cash) |

|---|---|---|

| Cash & Equivalents | Checking/Savings, Money Markets, Cash on hand, CDs | N/A |

| Investments | Publicly traded stocks, bonds, ETFs, mutual funds | Private equity, hedge funds, collectibles (art, wine) |

| Real Estate | N/A | Primary home, rental properties, vacation homes, land |

| Retirement Accounts | N/A (generally considered illiquid due to penalties) | 401(k)s, IRAs, Pensions |

| Personal Property | N/A | Vehicles, jewelry, antiques |

| Business Interests | N/A | Ownership in a private or family business |

Remember, the goal is to get a realistic picture of the funds you can tap into quickly in an emergency.

Tallying Up Your Short-Term Liabilities

Once you've got your list of liquid assets, it’s time to face the other side of the coin: your short-term liabilities. These are the debts you need to pay off within the next year or so. Be brutally honest here—underestimating what you owe will only give you a false, and dangerous, sense of security.

Your list of liabilities should include things like:

- Credit Card Balances: The full statement balance you owe, not just the minimum payment.

- Personal Loans: The outstanding balance on any loans from banks, credit unions, or online lenders.

- Auto Loans: The remaining principal you owe on your car.

- Student Loans: While it's a long-term debt, the portion due over the next 12 months can be relevant here.

- Any Other Short-Term Debt: This could be anything from medical bills and back taxes to a loan from a family member.

Notice we're not including the mortgage on your primary residence. Since we already excluded the house from the asset side of the equation, we leave the mortgage out of the liability side, too. The whole point is to compare your readily available cash against your most immediate financial obligations.

Putting It All Together: How Real Families Calculate Their Liquid Net Worth

Knowing the difference between liquid and illiquid assets is one thing, but the real magic happens when you apply the formula to your own life. It’s a simple calculation: Liquid Assets - Liabilities = Liquid Net Worth.

Let’s walk through a few stories that show how this simple number gives families the clarity they need to make smarter financial moves. These aren't just textbook examples; they reflect the messy, complicated, and very real situations many of us face.

Sarah, a Single Parent Building Her Safety Net

First up is Sarah, a single mom who just switched careers to create a more stable life for her two kids. After a few years of financial uncertainty, her top priority is building a solid safety net. Calculating her liquid net worth is the first step toward getting back in the driver's seat.

Here’s a quick look at her finances:

- Checking Account: $2,500

- High-Yield Savings (Emergency Fund): $8,000

- Investment Account (Stocks/ETFs): $15,000

- Credit Card Balance: $4,500

- Personal Loan: $3,000

Sarah first adds up her liquid assets: $2,500 + $8,000 + $15,000 comes out to $25,500. Then, she totals her liabilities: $4,500 + $3,000 for a total of $7,500.

Her liquid net worth is $18,000. For Sarah, this number is empowering. It confirms she has a respectable emergency fund in place and can now confidently shift her focus to tackling that high-interest credit card debt, which will directly boost her liquidity.

Mark and Lisa, the "Sandwich Generation" Couple

Next, let's look at Mark and Lisa, a couple in their early 50s. They're part of the "sandwich generation"—juggling their son's college tuition while also helping support Lisa's aging mother. For them, liquidity is all about being ready for the unexpected.

Their financial picture is a bit more complex:

- Joint Checking/Savings: $22,000

- Brokerage Account: $120,000

- Money Market Account (for elder care costs): $30,000

- Car Loans (both vehicles): $18,000

- Credit Card Balances: $7,000

Their liquid assets add up to $172,000 ($22,000 + $120,000 + $30,000). Their liabilities are $25,000 ($18,000 + $7,000).

This leaves Mark and Lisa with a liquid net worth of $147,000. That figure gives them peace of mind, knowing they can absorb a surprise medical bill for Lisa's mom or a tuition hike without raiding their long-term retirement accounts.

This quick visual guide can help you sort your own assets before you start crunching the numbers.

The main takeaway here is seeing the clear line between money you can use right away (liquid) and assets that are tied up (illiquid).

David and Maria, Planning for Retirement and Legacy

Finally, we have David and Maria, who are just five years out from retirement. They’re dreaming of traveling but also want to set up a financial legacy for their grandkids. They need to understand their immediate spending power, separate from their retirement nest egg.

Their finances include a mix of accounts:

- Savings Accounts: $75,000

- Taxable Investment Portfolio (Bonds & Stocks): $350,000

- HELOC Balance (from a recent remodel): $40,000

It’s important to note that we’re leaving their 401(k)s and IRAs out of this calculation since they can’t be tapped easily without penalties before retirement. Their liquid assets total $425,000 ($75,000 + $350,000), while their only major liability is the $40,000 HELOC.

David and Maria's liquid net worth stands at $385,000. This number shows them exactly how much capital they can work with for their immediate retirement goals without touching their long-term funds.

Calculating your liquid net worth isn't just an accounting exercise. It's about translating numbers on a page into a clear story about your family's financial resilience and freedom to make choices.

Think about it—sitting down and adding up the cash, stocks, and other assets you can access quickly, then subtracting any short-term debts. That final number is the financial heartbeat of your family's security. In my experience, it’s a critical metric for any family steward.

A recent report shows that the US holds a massive share of the world's liquid private wealth. This isn't just about big numbers; it's about prosperity that needs to be managed wisely. Calculating this metric isn’t for bragging rights—it’s about ensuring that wealth can flow smoothly when and where it's needed, even across generations. It’s a concept I call ‘Money Sends Messages.’ You can see more on these trends in the USA Wealth Report from Henley & Partners.

How to Interpret Your Liquid Net Worth

Alright, so you’ve crunched the numbers and have a figure in front of you. But what does that number actually tell you about where you stand? Your liquid net worth isn't just a static figure; it’s a living snapshot of your financial flexibility right now. Learning to read that snapshot is how you turn a simple calculation into a powerful tool for building real security.

Think of this number as your financial shock absorber. It’s what you have on hand to deal with life’s curveballs—both the good and the bad—without having to blow up your long-term plans. A sudden job loss, an emergency roof repair, or even a can't-miss investment opportunity all put your liquidity to the test.

What Is a Healthy Level of Liquidity?

A good rule of thumb is to aim for having 20% to 30% of your total net worth in liquid assets. This isn't a hard-and-fast rule, of course, but it’s a solid benchmark. It suggests you have enough cash and near-cash assets to handle surprises while your illiquid investments, like your home and retirement accounts, are left alone to grow.

It's all about finding the right balance:

- Too little liquidity can corner you into selling long-term investments at the worst possible moment or force you into high-interest debt just to cover a crisis.

- Too much liquidity, on the other hand, often means your money is just sitting there, not working for you. You could be missing out on significant long-term growth.

Striking that balance is where true financial peace of mind comes from. It's the confidence that comes from knowing you’ve got a cushion, ready for whatever life throws your way.

The real value of your liquid net worth isn't in the number itself, but in the freedom it gives you. It's the freedom to say "yes" to an opportunity or "I've got this" to a crisis, without hesitation.

This concept is especially critical for those of us building a legacy. For someone nearing retirement, knowing their liquid net worth is strong is incredibly empowering, and it’s part of a growing global trend. This "liquid gold" is what fuels smart strategies to make money last while also supporting your family’s dreams. This is particularly relevant in the US, which holds a huge piece of the worldwide wealth pie.

The timeless wisdom here is to focus on assets like stocks and bonds that can grow without tying your money down. You can dig deeper into these global wealth dynamics in the Allianz Global Wealth Report.

Ultimately, when you calculate liquid net worth, you're measuring your ability to stay in the driver's seat. This number directly reflects your power to seize opportunities, weather financial storms, and build the future you want for yourself and your loved ones.

Actionable Strategies to Boost Your Liquidity

If the number you calculated for your liquid net worth felt a little low for comfort, don't sweat it. The great news is this is one of those numbers you have direct control over. Bolstering your financial flexibility isn't about some drastic, overnight fix. It’s about a series of smart, intentional moves that create a much stronger foundation over time.

Forget the generic advice. Let's get into the practical steps you can start taking right away. These aren't just about puffing up a number on a spreadsheet; they're designed to give you genuine peace of mind, knowing you’re ready for whatever life throws your way. Each strategy tackles a key part of your financial picture, from savings and debt to your investments.

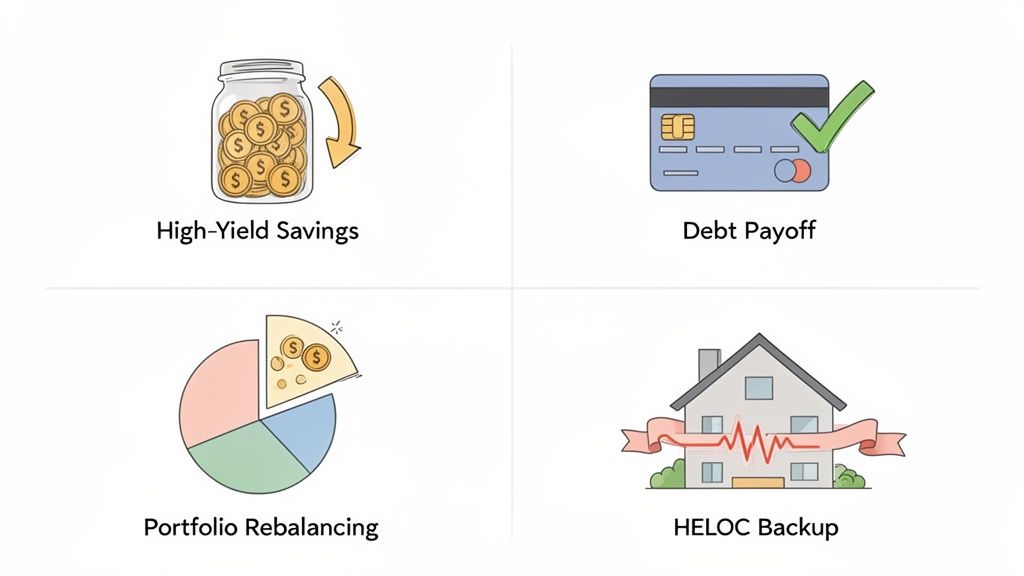

Build and Automate Your Emergency Savings

A rock-solid emergency fund is the bedrock of liquidity. I'm not talking about just any savings account, either. This needs to be a dedicated high-yield savings account (HYSA) that you keep completely separate from your day-to-day checking. That slightly higher interest rate puts your money to work, and keeping it separate makes it far less tempting to dip into for non-emergencies.

The absolute best way to build this fund is to put it on autopilot. Set up an automatic, recurring transfer from your checking to your HYSA right after every payday. Even if you start small, you're building a powerful habit. For a full breakdown, check out our emergency fund checklist with 8 must-have steps for true financial resilience.

The simple act of automating your savings is one of the most powerful messages you can send to your money. It says, 'My security comes first,' and puts your financial well-being on autopilot.

By consistently growing this cash cushion, you're directly pumping up the asset side of your liquid net worth equation. It's an immediate buffer against the unexpected.

Strategically Attack High-Interest Debt

Now for the other side of the equation: your liabilities. High-interest debt, especially the credit card kind, is an anchor dragging down your liquidity. Every single dollar you pay in interest is a dollar that could have been padding your savings or growing your investments. Knocking out this debt gives you an immediate and deeply satisfying boost to your liquid net worth.

Zero in on the debt with the highest interest rate first—this is often called the "avalanche" method—while just making the minimum payments on everything else. This approach saves you the most money in interest over the long haul. Once you've paid off one card, take that entire payment amount and roll it onto the next debt in line. You'll create a powerful snowball effect that accelerates your progress.

Rebalance Your Portfolio and Consider a HELOC

Your investment portfolio is another place to look for opportunities. You want to make sure you have a healthy mix of long-term growth assets and funds you can get to more easily. If your portfolio is too heavily weighted toward illiquid investments, it might be time to rebalance by increasing your holdings in things you can sell quickly, like stocks, bonds, or ETFs.

Finally, if you're a homeowner, a Home Equity Line of Credit (HELOC) can be a fantastic backup source of liquidity. Instead of being forced to sell your home in a crisis, a HELOC lets you borrow against your equity when you need it. You don't want to use it for frivolous spending, of course, but having that open line of credit can be an invaluable safety net for a true emergency, allowing you to keep your primary cash reserves untouched.

Your Questions About Liquid Net Worth Answered

Even after you've walked through the steps, it's totally normal to have a few questions rattling around. Nailing the details is the key to making sure the number you come up with is actually accurate and useful. Let's tackle some of the most common uncertainties I hear all the time.

Think of this as the final check-in before you put your new knowledge into practice. My goal is to clear up any lingering confusion so you can move forward with confidence.

Should I Include My Primary Home in This Calculation?

Nope, definitely not. Your primary home is a classic illiquid asset.

Sure, it holds a ton of value, but you can't turn that value into spendable cash overnight. You'd have to go through the whole drawn-out process of selling it. The entire point of calculating your liquid net worth is to see what you could get your hands on quickly in a pinch.

For this specific metric, stick to assets you can access within a few days without taking a major hit or penalty. Your home is a cornerstone of your total net worth, but it has no business in this particular calculation.

How Often Should I Calculate My Liquid Net Worth?

A good rhythm is to run the numbers every six to twelve months. That’s frequent enough to keep a solid pulse on your financial health without driving yourself crazy.

That said, you should absolutely recalculate it after any major life event. That includes things like:

- Starting a new job or getting a big raise

- Receiving an inheritance

- Taking on a new loan or finally paying one off

- Making a large purchase, like a new car

Doing these regular check-ins helps you see how you're progressing toward your goals and lets you make smart decisions based on your current reality, not last year's.

What Is the Difference Between Liquid and Total Net Worth?

This is a critical distinction, so let's make it crystal clear. Total net worth is the 30,000-foot view of your financial life. It includes all of your assets—both the liquid stuff (cash, stocks) and the illiquid stuff (your home, a business)—minus every single one of your liabilities.

Liquid net worth, on the other hand, is a specific slice of that picture. It hones in on only your liquid assets and pits them against your short-term liabilities. Think of total net worth as your entire financial story, while liquid net worth is the chapter covering your emergency fund and opportunity fund, all rolled into one.

Is It Possible to Have a Negative Liquid Net Worth?

Yes, absolutely. It's more common than you might think. If your short-term debts like credit card balances and personal loans add up to more than your easily accessible assets, your liquid net worth will be in the red.

This is a clear signal of a precarious financial position. It means you simply don't have the immediate resources to cover your current debts if you had to. While seeing a negative number can be a shock, it’s also an incredibly powerful wake-up call. It's the kick in the pants you might need to get serious about an aggressive debt-reduction strategy and start building up your savings.

At Smart Financial Lifestyle, we believe that understanding these key metrics is the first step toward making smarter financial decisions. To continue building your financial wisdom, explore more of our guides and resources. Learn more at smartfinancialifestyle.com.