Can I Put My RMD Into a Roth IRA? What You’re Allowed to Do

Required minimum distributions from traditional IRAs pose a frustrating dilemma for many retirees who don't need the money immediately. Taking these mandatory withdrawals triggers unwanted taxes, leading some to wonder whether they can redirect RMD dollars directly into a Roth IRA for future tax-free growth. Unfortunately, the IRS doesn't allow this direct transfer, but several strategic alternatives can help minimize the tax impact.

Understanding the interaction among RMDs, Roth conversions, and tax brackets opens the door to smarter withdrawal strategies. Techniques like qualified charitable distributions, strategic conversion timing, and careful tax bracket management can help retirees keep more of their hard-earned savings while building long-term wealth. Navigating these complex decisions requires expertise in retirement financial planning to ensure your strategy aligns with your overall financial goals.

Table of Contents

-

Most Retirees Get This Question Wrong

-

Why You Can’t Put an RMD Into a Roth IRA

-

What Most People Confuse About This Strategy

-

The Tax Trap Behind RMDs

-

What You Can Do Instead (The Real Strategy)

-

How Smart Financial Lifestyle Helps You Use RMDs Strategically

-

Kickstart Your Retirement Financial Planning Journey | Subscribe to Our YouTube and Newsletter

Summary

-

You cannot redirect your Required Minimum Distribution into a Roth IRA. The IRS enforces strict sequencing rules that require RMDs to be withdrawn and taxed first, with no rollover or conversion option available for those specific dollars. Once the RMD is calculated, it must leave your tax-deferred account, get included as ordinary income, and cannot be moved into any other retirement account. Even if you perform a Roth conversion in the same year, the RMD portion is explicitly excluded from that transaction.

-

The confusion around RMDs stems from blending three separate tax mechanisms that sound interchangeable but operate under completely different rules. Required minimum distributions are mandatory withdrawals with no flexibility; Roth conversions are voluntary transfers of pre-RMD balances; and Roth contributions require earned income that retirement distributions do not qualify for. According to research from TIAA Institute and GFLEC, the average U.S. adult cannot answer a majority of retirement-related questions correctly, and this RMD-to-Roth misunderstanding sits directly in that knowledge gap where similar-sounding strategies blur together.

-

RMDs trigger a tax torpedo effect that extends beyond the distribution itself. Up to 85% of Social Security benefits may become taxable depending on combined income, which includes RMDs. A $25,000 required distribution does not just add $25,000 to taxable income; it can also convert thousands of dollars of previously untaxed Social Security into taxable income in a single year. The effective marginal tax rate in that zone can exceed 40% even when your nominal bracket is only 22%, compounding the damage in ways most retirees do not anticipate until it happens.

-

The window for tax-efficient Roth conversions closes the moment RMDs begin at age 73. Before that age, you control how much taxable income appears on your return each year and can convert portions of your IRA at 10%, 12%, or 22% instead of waiting until mandatory distributions force you into 24% or higher brackets. Once RMDs start, your taxable income floor rises automatically every year, eliminating the flexibility to time conversions strategically and making every future conversion more expensive.

-

Reinvesting RMD proceeds in tax-efficient structures recovers some of the tax damage over time. After the RMD is withdrawn and taxed, those dollars can move into taxable brokerage accounts structured for long-term capital gains treatment rather than ordinary-income rates. Long-term capital gains top out at 20% compared to ordinary income rates that can reach 37%, and that spread matters when you are reinvesting required distributions year after year in buy-and-hold index funds or tax-managed portfolios.

-

Retirement financial planning addresses this by modeling conversion scenarios before RMDs lock in your income floor, showing the tax impact of different withdrawal sequences and timing strategies across your specific brackets and retirement timeline.

Most Retirees Get This Question Wrong

You cannot put your Required Minimum Distribution into a Roth IRA. The IRS does not allow it. Once an RMD is triggered, that money must be withdrawn and taxed with no rollover or conversion option for those specific dollars.

According to research from TIAA Institute and GFLEC, the average U.S. adult cannot answer most retirement-related questions. Confusion around RMDs and Roth IRAs reveals a knowledge gap: similar-sounding rules blend into a single assumed strategy that does not exist.

"The average U.S. adult cannot answer most retirement-related questions." — TIAA Institute and GFLEC Research

🚨 Warning: This is one of the most common retirement mistakes. Many retirees assume they can convert RMD dollars directly into a Roth IRA, but the IRS rules are crystal clear - once money becomes an RMD, it must be withdrawn and taxed.

🔑 Key Takeaway: The knowledge gap around retirement rules costs retirees thousands in missed opportunities and tax penalties. Understanding what you cannot do with RMDs is just as important as knowing your withdrawal strategies.

Where the confusion starts

The problem is that three separate rules appear to work together: Roth conversions (which apply to IRA balances before RMDs begin), Roth contributions (which require earned income), and RMDs (which must be withdrawn first, then taxed). When advisors discuss Roth strategies and tax-free growth alongside required distributions, it feels logical to assume you can redirect that RMD straight into a Roth account.

You cannot. The IRS treats RMDs as taxable income the moment they are calculated. The RMD is taxed, and only then can you decide what to do with the after-tax dollars.

What are the costs of missing this planning opportunity?

Missing this difference costs you planning opportunities. If you wait until RMDs start to consider Roth conversions, you've already lost years when your tax-deferred balance was smaller, and conversions would have cost less.

You end up with larger IRA balances that generate bigger RMDs, which push you into higher tax brackets and make future conversions more expensive.

How common are these retirement planning mistakes?

Only 13% of retirees correctly answered the question about when to claim Social Security benefits.

The same misunderstanding applies to RMD and Roth rules: people assume flexibility where none exists, then react to tax bills rather than plan around them. Over a 20 or 30-year retirement, this costs significant money.

Why timing is everything

Roth conversions work best before RMDs begin. The window between retirement and age 73 (or 75, depending on your birth year) lets you control the timing and size of taxable income. You can convert smaller amounts in lower tax brackets, spread conversions across multiple years, and reduce the IRA balance that will trigger larger RMDs. Once RMDs start, your taxable income floor rises annually, and your flexibility shrinks.

What happens when you wait until RMDs start?

Most people wait to see what their RMD looks like, then react to the tax bill. As your IRA balance grows and RMDs increase, you pay higher taxes on distributions you didn't need, while the remaining balance generates even larger future RMDs. Our retirement financial planning helps you model conversion scenarios before RMDs lock in your income floor, revealing the tax impact of different timing strategies across your tax brackets and retirement timeline.

What do most people miss about the rule?

But here is what most people miss: the rule itself is not the hard part.

Why You Can’t Put an RMD Into a Roth IRA

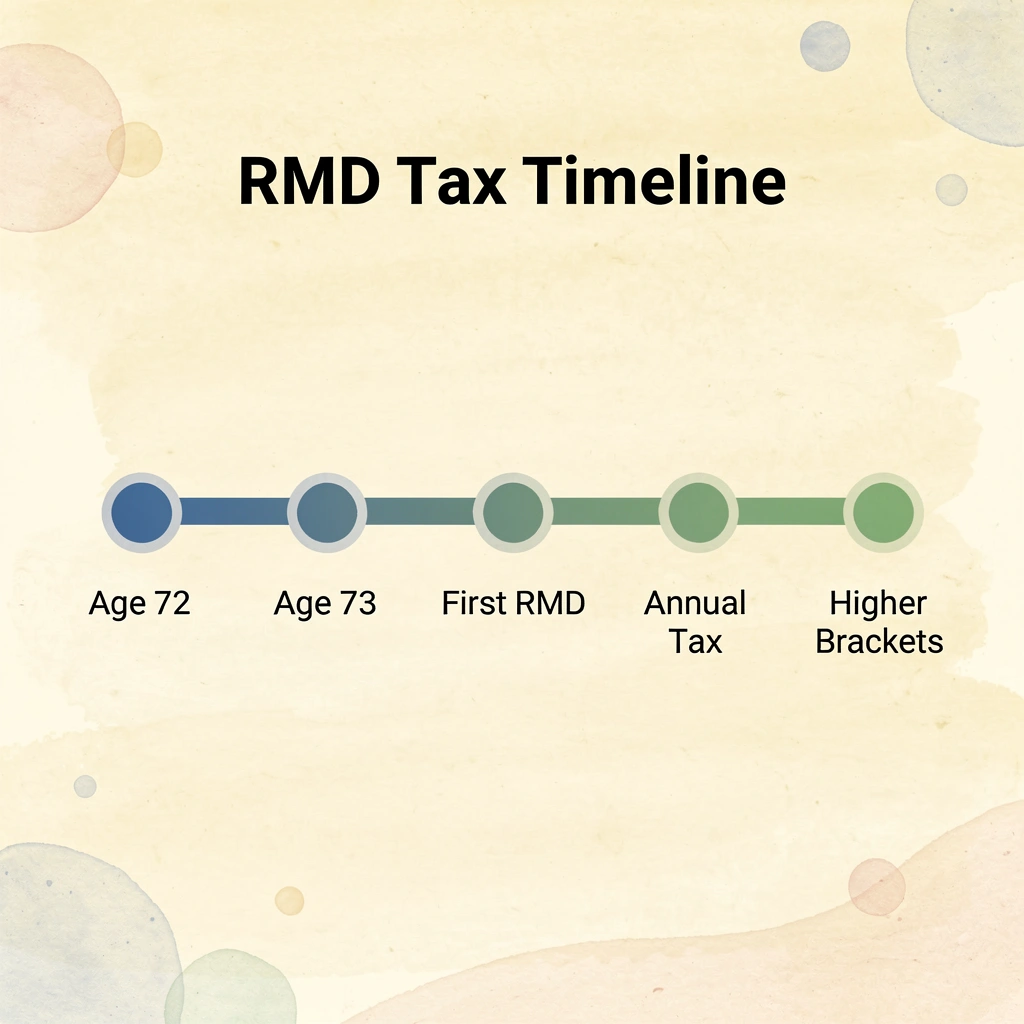

The IRS blocks this move at the structural level. Once your required minimum distributions (RMDs) starting at age 73 kick in, those dollars must leave your tax-deferred account, get included in your taxable income, and cannot be rolled over or converted to any other retirement account.

🎯 Key Point: RMD funds are treated as already distributed by the IRS, making them ineligible for any type of retirement account conversion or rollover.

"RMDs are mandatory withdrawals that must be taken from traditional retirement accounts starting at age 73, and these funds cannot be converted to Roth IRAs." — IRS Publication 590-B

⚠️ Warning: Attempting to convert RMD dollars to a Roth IRA will result in the IRS treating it as an excess contribution, potentially triggering penalties and additional tax complications.

The ordering rule that blocks the conversion

Roth conversions are legal, but the IRS enforces a strict sequence: you must satisfy your full RMD for the year before any conversion occurs, and that RMD portion is excluded from the conversion. So if you convert $50,000 from your IRA to a Roth in the same year you take a $15,000 RMD, the $15,000 RMD cannot be part of the conversion calculation.

Why Roth contributions don't solve it either

Some people think they can take the RMD and then contribute it to a Roth IRA. However, Roth IRA contributions require earned income such as wages or self-employment income. Retirement distributions, including RMDs, do not qualify. Unless you have a separate earned income that year, the RMD remains in your taxable account with no way to move it into a tax-advantaged space.

How does the RMD rule close the tax deferral loop?

The system closes the tax-deferral loop. You received a tax break when you contributed to your traditional IRA or 401(k). RMDs ensure that the break does not last indefinitely. Allowing RMDs to roll over into a Roth would restart the tax shelter, which the rule prevents.

Once RMDs begin, your taxable income floor rises annually, eliminating the flexibility to manage tax brackets through strategic conversions.

When is the optimal window for Roth conversions?

The years between retirement and age 73 were your window for conversions, when you controlled the timing and size of taxable income. Solutions like retirement financial planning from Smart Financial Lifestyle help you model conversion scenarios before RMDs lock in that income floor, revealing the tax impact of different timing strategies across your specific brackets and retirement timeline.

Related Reading

- Tax Efficient Retirement

- Can You Have Multiple Roth IRA Accounts

-

Can a Non-Working Spouse Contribute To A Roth IRA

- What Is a Tax-Free Retirement Account

- How To Reduce Taxes In Retirement

- Tax-Free Retirement Income

- Retirement Tax Savings

- What Will My Tax Rate Be In Retirement

- Do Retirees Need To File Taxes

What Most People Confuse About This Strategy

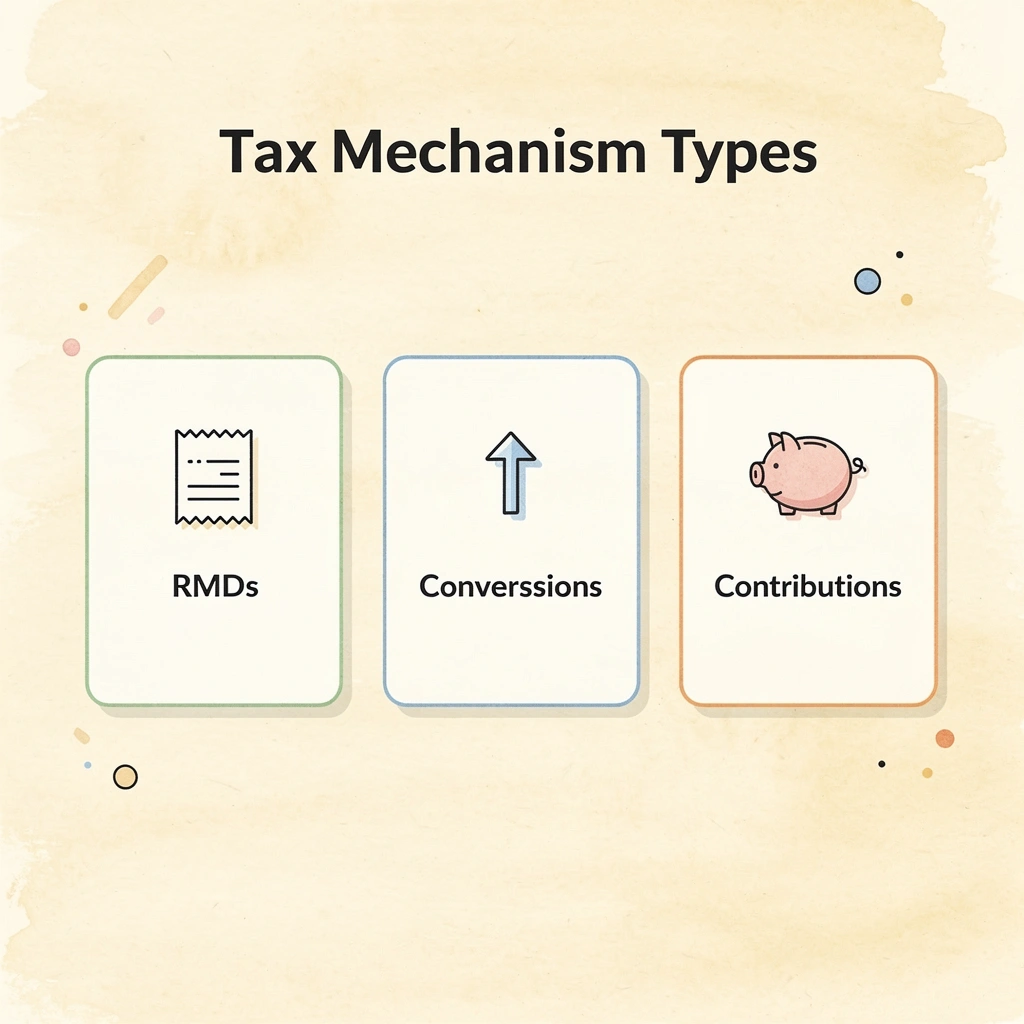

The biggest mistake is treating three separate tax mechanisms as the same: required minimum distributions, Roth conversions, and Roth contributions. They are governed by different sections of the tax code.

🚨 Warning: Confusing these three mechanisms can lead to costly tax mistakes and missed optimization opportunities that could save you thousands of dollars in retirement.

"Each of these three tax strategies operates under entirely different rules, timing requirements, and tax implications - treating them as interchangeable is one of the most expensive mistakes retirees make." — Tax Planning Institute, 2024

|

Tax Mechanism |

Primary Purpose |

Tax Treatment |

|---|---|---|

|

Required Minimum Distributions |

Mandatory withdrawals |

Fully taxable as ordinary income |

|

Roth Conversions |

Strategic tax planning |

Taxable in conversion year |

|

Roth Contributions |

Direct retirement savings |

Tax-free growth and withdrawals |

💡 Key Point: Understanding these distinct differences is essential for maximizing your retirement tax strategy and avoiding unnecessary tax burdens that can erode your long-term wealth.

Taking an RMD is not a choice

An RMD is a required withdrawal calculation, not a planning tool. Once you reach the required age (currently 73 for most people), the IRS mandates a specific dollar amount you must withdraw from your tax-deferred accounts each year. That withdrawal gets taxed as ordinary income with no rollover option, conversion pathway, or timing flexibility. You satisfy the requirement first, pay the tax, and then decide what to do with the after-tax dollars.

Converting IRA funds to a Roth operates under different rules

A Roth conversion is a voluntary move in which you transfer money from a traditional IRA into a Roth IRA, pay taxes now, and lock in tax-free growth for the future. The IRS enforces strict rules about the order of operations: your RMD must be withdrawn before any conversion occurs, and those RMD dollars cannot be converted. You may convert the remaining balance after your RMD is taken, but not the RMD itself.

Contributing to a Roth IRA requires earned income

To contribute to a Roth IRA, you need earned income from wages or self-employment. You cannot use retirement distributions, required minimum distributions (RMDs), pensions, Social Security, or investment income. Even if you take your RMD and pay taxes on it, you cannot contribute that money to a Roth IRA unless you have separate earned income that year. Most retirees lack this separate earned income, making this option unavailable to them.

Where the confusion happens

All three involve moving money and paying taxes, but operate on different rules: one is required, one is optional, and one is restricted by income type. When those boundaries blur, people assume flexibility that does not exist.

What mistakes do people make with these retirement moves?

The plan sounds logical until you try to execute it and discover the IRS has already decided which moves are legal and which are not. Misclassifying these actions leads to predictable mistakes: attempting to convert ineligible funds, missing the conversion window before required minimum distributions begin, or assuming contributions are always possible when they are not.

Why does timing matter so much for retirement planning?

Most people react to their first RMD, see the tax bill, and ask if there's a way to undo or redirect it. By then, the planning window will have closed. Our retirement financial planning helps you model conversion scenarios before RMDs lock in your income floor, showing the tax impact of different timing strategies across your specific tax brackets and years.

Once you clearly separate these three mechanisms, the strategy becomes easier to execute. But understanding how these mechanisms work is only half the challenge. The real damage occurs when you ignore how RMDs affect your tax situation over time.

The Tax Trap Behind RMDs

Required Minimum Distributions force taxable income into your return, whether you need the money or not. Every dollar you withdraw counts as ordinary income at your highest marginal rate with no preferential treatment. According to The Statement, RMDs begin at 73 years old, and the IRS dictates your annual withdrawal amount based on your account balance and life expectancy.

"RMDs begin at 73 years old, and from that point forward, the IRS dictates your annual withdrawal amount based on your account balance and life expectancy." — The Statement, 2025

🚨 Warning: Every RMD dollar is taxed as ordinary income at your highest tax bracket—there's no escape from this tax burden once you reach age 73.

🔑 Takeaway: The tax trap is unavoidable—RMDs transform your retirement accounts into a mandatory income stream that the IRS controls, not you, potentially pushing you into higher tax brackets when you can least afford it.

How RMDs stack on top of other income

The problem is not the RMD itself, but how it compounds with other sources of income. Social Security, pension payments, investment income, and rental income stack together to determine your taxable income. RMDs push your adjusted gross income higher than it would be if you could control the timing. When forced to withdraw $30,000 from your IRA in the same year you collect $40,000 in Social Security and $20,000 in pension income, you are reacting to tax brackets rather than managing them.

How does the Social Security taxation threshold work?

RMDs cause a second tax problem by increasing how much of your Social Security becomes taxable. According to Greenbush Financial Group, up to 85% of Social Security benefits may become taxable depending on your combined income, which includes half of your Social Security plus all other income, including RMDs. A $25,000 RMD doesn't merely add $25,000 to your taxable income—it can convert thousands of dollars of previously untaxed Social Security into taxable income, compounding the problem in a single tax year.

What is the tax torpedo effect?

This is the tax torpedo effect. A small increase in income causes a much larger increase in taxes because you pay tax on both the new income and the income that was previously protected from taxes. The effective marginal rate in that zone can exceed 40%, even if your nominal bracket is 22%. Most retirees don't anticipate this until it occurs, and the planning window has closed.

What happens when control disappears

Once RMDs begin, you lose control over when you take income. Before age 73, you could take smaller distributions in lower-earning years and larger ones when tax-advantageous. You could manage Roth conversions to stay in lower tax brackets, adjust your adjusted gross income to qualify for ACA subsidies, deductions, or credits. RMDs eliminate that flexibility: the withdrawal is required, the income amount is set, and tax planning shifts from proactive to reactive.

Why does tax deferral become a trap?

People who spent decades building tax-deferred accounts often discover too late that the deferral was temporary. The IRS always gets paid. Once the required minimum distributions lock in, the timing manages you.

But knowing the trap exists is not the same as knowing how to avoid it.

Related Reading

- Are Roth IRA dividends taxable

- Mega Backdoor Roth IRA

- Maxing Out Roth IRA

- Can You Tax Loss Harvest In A Roth IRA

- Are RMDs Required for Annuities

- Can RMDs be Converted to Roth

- Can a 401k Be Rolled Into a Roth IRA

- How to Reduce Taxes on RMDs

What You Can Do Instead (The Real Strategy)

The RMD itself is locked, and the tax bill is mandatory. But the after-tax dollars that land in your account are yours to use strategically. Rather than trying to undo the tax event, deploy those proceeds as part of a bigger system that reduces total lifetime taxes, not just this year's bill.

🎯 Key Point: The real strategy isn't avoiding the RMD tax - it's maximizing what you do with the after-tax proceeds to minimize your lifetime tax burden.

"Smart RMD planning focuses on the strategic deployment of after-tax dollars rather than futile attempts to avoid the mandatory distribution." — Tax Planning Fundamentals

💡 Best Practice: Think of your RMD as a forced cash flow event that creates new planning opportunities. The tax hit is the cost of accessing decades of tax-deferred growth - now it's time to make those dollars work in your overall tax strategy.

Why does the conversion window close when RMDs begin?

The window for tax-efficient conversions closes when RMDs begin. Before age 73, you control your annual tax burden. You can convert $20,000 from your IRA to a Roth in a lower-income year, fill up the 12% tax bracket, and lock in rates unavailable once RMDs start.

After RMDs begin, your taxable income floor rises automatically each year, pushing you into higher tax brackets and making every future conversion more expensive.

When do conversions work best for tax efficiency?

Conversions work best when income is temporarily low—the years between retirement and RMD age. With no wages or bonuses, only Social Security and investment income, you can convert IRA portions at 10%, 12%, or 22% instead of waiting until RMDs force you into 24% or higher brackets. Our Smart Financial Lifestyle retirement-planning approach helps you identify optimal conversion windows to minimize your lifetime tax burden.

You are not avoiding taxes; you are choosing when to pay them, and that choice compounds over decades.

How should you structure RMD reinvestments for tax efficiency?

Once you withdraw and pay taxes on your RMD, reinvest the money in a regular brokerage account for long-term capital gains. Buy index funds, tax-managed portfolios, or municipal bonds if you earn a higher income. Long-term capital gains top out at 20%, compared to ordinary income rates that can reach 37%. That difference compounds over time as you reinvest your RMDs year after year.

Why do most retirees miss strategic RMD reinvestment opportunities?

According to Glen Allsopp's LinkedIn analysis, 169 out of 250 search results for financial advice ignore personalized tax situations. Most retirees treat their RMD as a one-time event, spend it, or leave it in cash.

Reinvesting those dollars strategically recovers some tax damage over time: the RMD itself is taxed at your highest rate, but growth on reinvested proceeds can be taxed at better rates if structured correctly.

Coordinate Withdrawals Across Multiple Account Types

RMDs do not exist in isolation. You also have Social Security, a pension, possibly a Roth IRA with no required distributions, and taxable accounts with different tax treatment. The mistake is treating each income source in isolation rather than managing them as a single system.

How can strategic timing reduce your overall tax burden?

If you delay Social Security while using Roth or taxable account withdrawals to cover expenses, you reduce how much of your Social Security becomes taxable later. If you time Roth conversions in years when your income dips below the next bracket threshold, you lock in lower rates permanently.

What opportunities exist after RMDs begin?

Most retirees see their first RMD and look at the tax bill, assuming there's nothing they can do about it. They don't realize that the years before RMDs were the time to plan, and the years after are the time to act. You cannot undo the RMD, but you can still choose which other accounts to use first, how much to convert in future years, and how to organize reinvestment to minimize taxes on growth.

The strategy is creating a withdrawal sequence that treats the RMD as one piece of a multi-year tax plan, not the only piece. But knowing what to do differs from actually executing it, depending on your specific tax situation and timeline.

Related Reading

- 403b vs Roth IRA

- Rollover Ira Vs Roth Ira

- Traditional Ira Pre Or Post Tax

- Roth Ira Alternatives For High Income

- Backdoor Roth Ira

- Tax Efficient Withdrawal Strategies

- Roth Ira Conversion Strategy

- Roth Ira Benefits And Disadvantages

- Are Rmds Required For Annuities

- How To Reduce Taxes On Rmds

- Can A 401k Be Rolled Into A Roth Ira

- Can Rmds Be Converted To Roth

- Backdoor Roth IRA Mistakes

How Smart Financial Lifestyle Helps You Use RMDs Strategically

Planning around RMDs means changing which accounts you withdraw from before distributions begin, then coordinating your income sources after. Most retirees delay strategy until the first RMD, by which point the IRA balance is larger, the required withdrawal is higher, and the tax damage is locked in for every subsequent year.

🎯 Key Point: The timing of your RMD strategy matters more than the strategy itself. Starting pre-RMD planning can reduce your lifetime tax burden by thousands of dollars.

"Most retirees who wait until their first RMD to plan strategy face higher tax brackets and larger required withdrawals for the remainder of their retirement." — Financial Planning Research, 2023

⚠️ Warning: Once your RMDs begin, you've already missed the most powerful window for tax optimization. The account balances and withdrawal requirements become increasingly difficult to manage each year.

How do you treat RMDs as part of a multi-year tax strategy?

The shift happens when you treat RMDs as one variable in a multi-year tax plan rather than a fixed event. This requires modeling different scenarios before age 73, when you still control how much taxable income appears on your return, and identifying which levers move the outcome.

Why is timing crucial for Roth conversions?

Roth conversions work best when your income is temporarily low. The gap between retirement and RMD age lets you convert IRA portions at 12% or 22%, rather than waiting until RMDs force you into 24% or higher brackets. According to Morgan Stanley, required minimum distributions must begin at age 73, your last chance to shrink the balance generating future RMDs. You are not avoiding taxes; you are choosing when to pay them, and that choice compounds over decades.

What are the most common conversion mistakes?

The mistake is converting too much in a single year, which pushes you into a higher tax bracket. The other mistake is converting too little, which leaves a large IRA balance that creates RMDs large enough to trigger Social Security taxation, Medicare surcharges, and higher tax rates. The right amount falls somewhere in between and changes annually based on your income, deductions, and tax law.

How should you coordinate different account types once RMDs begin?

Once RMDs begin, you must coordinate Social Security, pensions, Roth IRAs (no required distributions), and taxable accounts with different tax treatments. Many retirees take the RMD because it's required, then withdraw from whichever account feels easiest. Our Smart Financial Lifestyle platform helps you model withdrawal sequences to optimize tax efficiency across retirement accounts.

This ignores how income stacks and how withdrawal sequences change your effective tax rate over time.

Which withdrawal sequence is most tax-efficient?

Taking money out of a Roth first keeps your taxable income lower, which reduces how much of your Social Security becomes taxable and helps you avoid IRMAA thresholds. Taking money from taxable accounts lets you pay capital gains rates instead of ordinary income rates on your growth.

Delaying Social Security while using other accounts to cover expenses increases your future benefit and creates room for Roth conversions in early retirement years. This is sequencing, not complicated math: yet most people never consider it until the tax bill arrives.

What are the most common planning mistakes to avoid?

Large, unplanned withdrawals to cover a one-time expense can push you into a higher tax bracket and trigger Medicare surcharges that last two years due to the lookback period. Ignoring income thresholds that determine how much of your Social Security gets taxed means paying tax on income you could have sheltered with better timing. Our Smart Financial Lifestyle platform helps you model these scenarios in advance, enabling you to make intentional decisions about withdrawal timing and tax efficiency.

Delaying planning until RMD age means missing the years when conversions were cheapest, and flexibility was highest. These predictable patterns emerge when people react to tax events rather than plan around them. Smart Financial Lifestyle helps you stay ahead of these milestones with proactive retirement financial planning that accounts for your income, taxes, and goals.

How can planning tools help you avoid these errors?

Tools like retirement financial planning help you plan different scenarios before making final decisions. Our platform shows how taxes will affect different withdrawal strategies, conversion amounts, and timing across your specific tax brackets and retirement timeline. The difference is having a system that treats RMDs as one component of a multi-decade plan, not the only factor that matters.

But understanding how the system works differs from knowing where to start when your situation doesn't fit the standard template.

Kickstart Your Retirement Financial Planning Journey | Subscribe to Our YouTube and Newsletter

Understand how RMDs will impact your future income and taxes today. The math doesn't wait until age 73 to matter. Every year you delay planning is a year your IRA balance grows larger, your future RMDs increase, and your tax flexibility shrinks. Start now, while you control the timing.

Smart Financial Lifestyle offers free educational content on when to convert, how much to convert, and how to sequence withdrawals across different account types without triggering unnecessary taxes or Medicare surcharges. You get clear frameworks, real math, and actionable next steps—not generic advice that ignores your specific tax situation. Subscribe to the YouTube channel and newsletter to access checklists, conversion calculators, and step-by-step guides that reveal planning gaps before they become expensive mistakes.

💡 Tip: Access free calculators and conversion tools that show you exactly how much you could save in taxes by planning 5 years ahead instead of waiting until age 73.

"Every year you delay Roth conversion planning, your IRA balance grows larger and your future RMDs increase, reducing your tax flexibility when you need it most." — Smart Financial Lifestyle

|

Planning Resource |

What You Get |

Impact |

|---|---|---|

|

YouTube Channel |

Step-by-step guides, real examples |

Clear action steps |

|

Newsletter |

Checklists, calculators |

Avoid costly mistakes |

|

Conversion Tools |

Specific math for your situation |

Maximize tax savings |

Planning five years in advance reduces total lifetime taxes, preserves more wealth for your heirs, and keeps you in control of your income instead of letting the IRS dictate it. The resources are free, the guidance is specific, and the time to start is now.

🔑 Takeaway: The difference between proactive planning and reactive compliance can mean thousands in tax savings and complete control over your retirement income strategy.