Your Guide to Retirement Asset Allocation by Age

Retirement asset allocation by age is a simple but powerful idea: you adjust your investment mix based on where you are in life. The goal is to shift from a portfolio built for aggressive growth when you're young to one focused on stability and income as you get closer to retirement.

Think of it as planning a long journey. When you have decades ahead of you, you can afford to take some scenic, exciting routes that might have a few bumps but offer incredible views. As you near your destination, though, you switch to the safest, most direct highway to make sure you arrive on time and without any trouble. This strategy is all about managing risk while giving your portfolio the best chance to grow.

Charting Your Course with an Age-Based Financial Roadmap

Planning for retirement really is like that cross-country road trip. In your 20s, you’ve got a full tank of gas and a long road ahead. You can take those adventurous, high-growth detours—and in financial terms, that means a portfolio loaded up with stocks. These investments have the highest potential for big returns, but they also come with more volatility, just like a winding mountain pass.

As you get closer to your destination—retirement—your priorities naturally change. You wouldn't risk getting lost or running out of fuel just a few miles from the finish line, right? Of course not. You’d get on the most reliable and direct highway to guarantee a safe arrival. This is where bonds and other stable assets come into play. They offer lower risk and more predictable returns, preserving the wealth you've worked so hard to build.

The Two Engines of Your Portfolio

At its heart, age-based asset allocation is about managing the two main engines of your investment vehicle:

- Stocks (The Growth Engine): Think of stocks as the powerful engine that drives your portfolio forward. They represent ownership in a company and are designed for long-term growth, helping your money outpace inflation and build serious wealth over many years.

- Bonds (The Stability Engine): Bonds are more like the braking and suspension system. They are essentially loans you make to a government or corporation for a steady stream of interest payments. They provide stability and income, smoothing out the ride during those inevitable bumpy market conditions.

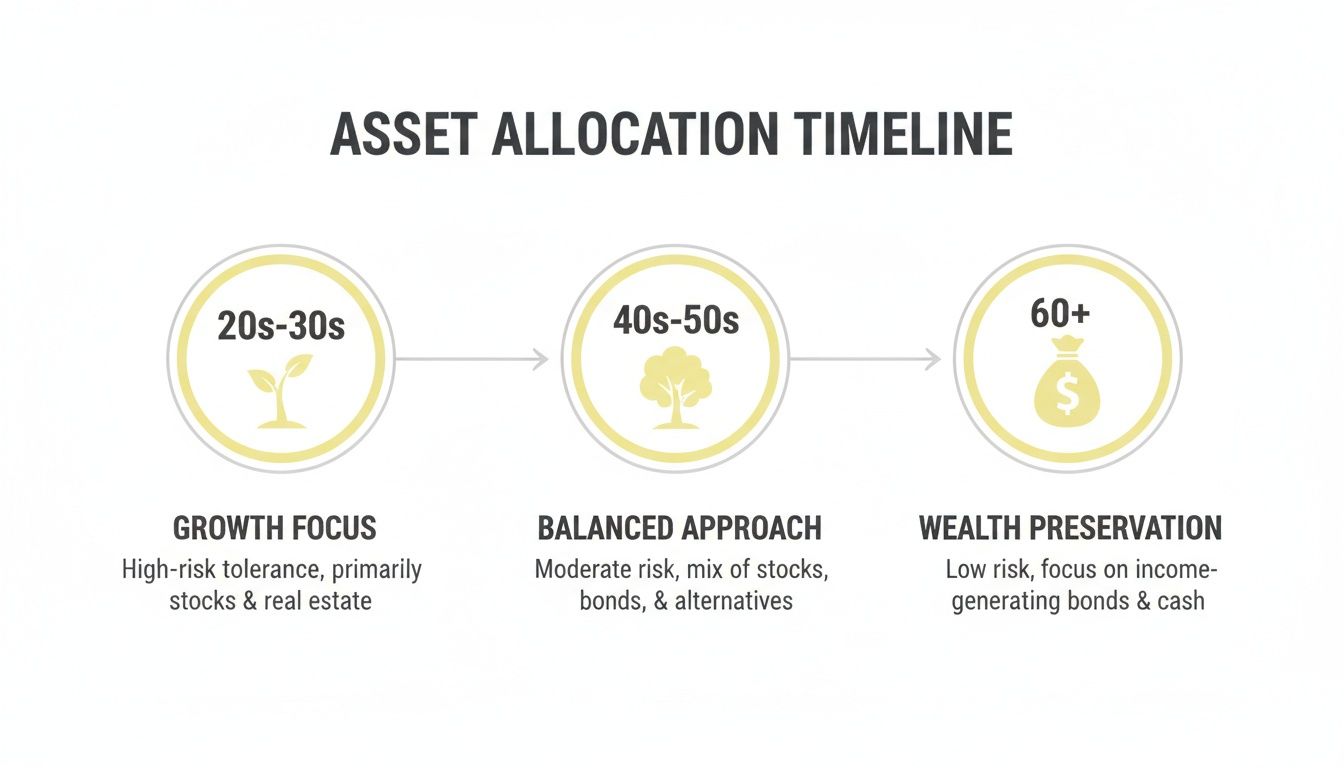

This timeline gives you a great visual of how your investment mix should evolve over your lifetime, shifting from aggressive growth to capital preservation.

The key takeaway is that your strategy changes over time. You start by building wealth in your early years, then you pivot to protecting it as you get ready to live off your savings. It’s a simple concept, but it's the one that connects your financial decisions to your real-life goals, whether that’s funding a comfortable retirement, taking care of family, or leaving a meaningful legacy.

To make this more concrete, here's a look at how a typical asset allocation "glidepath" might look as you move through different decades of your life.

Sample Asset Allocation Glidepath by Decade

| Age Range | Recommended Stock Allocation % | Recommended Bond & Cash Allocation % | Primary Goal |

|---|---|---|---|

| 20s–30s | 80% - 100% | 0% - 20% | Aggressive Growth |

| 40s | 70% - 85% | 15% - 30% | Growth & Accumulation |

| 50s | 50% - 65% | 35% - 50% | Balanced Growth |

| 60s+ | 30% - 50% | 50% - 70% | Preservation & Income |

This table is just a starting point, of course. Your personal situation, risk tolerance, and specific goals will always be the most important factors. However, it provides a clear picture of the fundamental principle: your portfolio should gradually become more conservative as your time horizon shortens.

The Growth Years: Your Strategy in Your 20s and 30s

When you’re in your 20s and 30s, you have a financial superpower that you can never get back later in life: time. With decades between you and retirement, you’re in the perfect position to harness the incredible power of compounding growth. This is the time to be bold, take on calculated risk, and lay a powerful foundation for your financial future.

Think of your investment portfolio like a tiny sapling. Your job right now isn't to harvest its fruit; it's to give it the richest fertilizer possible so it can grow into a mighty tree. For your portfolio, that fertilizer is a heavy dose of stocks.

Why an Aggressive Strategy Makes Sense

For this stage of life, an aggressive retirement asset allocation by age means putting a significant chunk of your money into stocks—often in the 80-90% range. That might sound risky, but it’s actually a savvy, strategic move. Why? Because stocks have historically delivered much higher long-term returns than bonds, and your long time horizon acts as a powerful shock absorber for market ups and downs.

A market downturn, which can feel scary, is actually a golden opportunity for you. When stock prices drop, your regular contributions buy more shares at a discount. It’s like your favorite store having a massive sale—you get more for your money, setting yourself up for even bigger gains when the market bounces back.

"A market downturn is the single biggest wealth-generating opportunity for a young investor. By continuing to invest consistently, you're not just weathering a storm; you're actively sowing the seeds for a much larger harvest down the road."

This aggressive approach is what fuels your major life goals. The growth you capture in these early years can become the down payment on a house, funding for your kids' education, or even the ticket to retiring years ahead of schedule. Starting with confidence is everything; if you're just getting started, our guide on how to start investing for beginners can help.

Applying a Simple Rule of Thumb

A great, simple starting point is the classic "100 Minus Age" rule. It’s exactly what it sounds like: subtract your age from 100 to figure out the percentage of your portfolio that should be in stocks.

- At age 25: 100 - 25 = 75% in stocks

- At age 35: 100 - 35 = 65% in stocks

This simple guideline gives you a clear, logical reason for a stock-heavy portfolio. As financial veteran Paul Mauro, with his 50+ years of experience, often says, aligning your money with your life's timeline is the first step toward smart financial decisions.

Some experts even push for a more aggressive stance for young investors. Charles Schwab, for instance, suggests that investors with over 15 years until retirement could allocate up to 95% to stocks. The reasoning is solid: stocks have historically outpaced both inflation and bonds, allowing your nest egg to compound far more effectively.

Ultimately, the goal in your 20s and 30s is crystal clear: maximize growth. By embracing a stock-focused portfolio, you put your greatest asset—time—to work building a powerful financial engine that will serve you for the rest of your life.

The Balancing Act Navigating Your 40s and 50s

Hitting your 40s and 50s can feel like a financial juggling act. You’re likely in your peak earning years, which is fantastic, but that income is often stretched thin. You might find yourself sandwiched between paying for your kids' college, chipping away at a mortgage, and helping care for aging parents.

That aggressive, growth-at-all-costs strategy from your 20s and 30s probably doesn't feel quite right anymore. This is the time to shift from pure accumulation to a smarter blend of growth and preservation. Your goal is to keep your nest egg growing ahead of inflation, but also to protect the capital you’ve worked so hard to build. The finish line is finally in sight, so avoiding a major setback is crucial.

Shifting Gears Toward Stability

So, what does this strategic shift look like in practice? It's all about gradually dialing back your stock exposure and increasing your allocation to bonds. Think of it like taking your foot off the accelerator as you approach a turn on the highway—you’re not stopping, just preparing for what’s ahead.

A common recommendation for this life stage is to aim for a portfolio of 60-70% stocks and 30-40% bonds. This mix keeps a solid majority in growth-oriented assets while providing a substantial cushion to soften the blow of market volatility. This thoughtful balance is a cornerstone of a successful retirement asset allocation by age.

This balanced approach is especially important for women in transition who might be rebuilding after a divorce, or family stewards managing multi-generational needs. The stability from a higher bond allocation offers peace of mind when you simply can't afford a major financial disruption.

Updating Old Rules for a New Reality

You've probably heard of the classic "100 Minus Age" rule for stock allocation. But with people living longer and markets changing, that old rule of thumb is a bit dated. A more modern guideline is the "120 Minus Age" rule, which suggests keeping a bit more in stocks.

A more modern approach, the '120 Minus Age' rule, acknowledges that we're living longer and need our investments to keep growing. This simple formula helps you maintain the growth needed to fund a potentially 30-year retirement.

Using this updated model, your allocation might look more like this:

- At age 45: 120 - 45 = 75% in stocks

- At age 55: 120 - 55 = 65% in stocks

This gradual reduction helps shield your portfolio as your investment timeline gets shorter. As expert Paul Mauro’s wisdom suggests, the key is a smart transition that balances upside with protection. For a deeper dive into this pivotal decade, check out our guide on how to prepare for retirement in your 50s.

Major financial institutions echo this balanced sentiment. Charles Schwab, for example, suggests a moderate investor about 10 years from retirement might hold 60% stocks, 35% bonds, and 5% cash. T. Rowe Price has also set some helpful benchmarks, recommending you have 5 times your income saved by age 50 and 7 times by age 55. These numbers highlight the importance of both consistent saving and a well-calibrated investment mix during these critical years.

Preservation And Income: Your Strategy In Your 60s And Beyond

Once you hit your 60s and the retirement finish line is in sight, your entire financial mindset needs to do a 180. The long race for growth is pretty much over. Now, the name of the game is protecting the wealth you’ve worked so hard to build and turning it into a reliable stream of income that will see you through the rest of your life.

This new chapter is all about preservation and predictability. The biggest risk isn’t missing out on the next hot stock anymore; it’s taking a major hit right when you’re about to start tapping into your savings. A nasty market downturn in your first few years of retirement can be devastating, which is why a more conservative retirement asset allocation by age becomes absolutely critical.

Building A Durable Financial Engine For Retirement

To get that stability, the typical portfolio for someone in their 60s (and beyond) tilts heavily toward fixed-income investments. A common mix is somewhere around 30-50% in stocks and 50-70% in bonds and cash. This setup is designed to do two very important jobs:

- Protect Your Principal: That large chunk of bonds acts like a giant shock absorber, shielding the bulk of your portfolio from the stock market's wild swings.

- Generate Consistent Income: Bonds and similar investments kick off predictable interest payments, creating a steady flow of cash you can use to cover your bills.

This isn't about being timid with your money; it’s about being smart. It’s about setting yourself up with the financial freedom to actually enjoy retirement without constantly stressing over market headlines.

Navigating The Practicalities Of Retirement Income

With this more conservative allocation locked in, your focus shifts to the day-to-day management of your money. Two big things come into play here: creating reliable income streams and dealing with Required Minimum Distributions (RMDs).

You'll need a solid strategy for turning that nest egg into a regular "paycheck." This usually means piecing together income from a few different places, like Social Security, any pensions you might have, and planned withdrawals from your investment accounts. We get into the nuts and bolts of this in our definitive guide to retirement income.

Then, once you turn 73, Uncle Sam steps in. The IRS requires you to start taking RMDs from most of your retirement accounts. These withdrawals aren't optional, and they're calculated based on your account balance and life expectancy. Getting a plan in place for RMDs is a must for managing your income and tax bill.

"In retirement, your portfolio is no longer just a measure of wealth; it's your personal salary and benefits package. The goal is to create a structure so reliable that you can focus on your life, not your account balance."

My own 50+ years of experience have taught me a clear lesson for this stage: prioritize preservation. A portfolio of 30-40% stocks and 50-60% bonds, with a bit of cash on the side, is a sensible approach. This lines up with what major firms like Schwab recommend, often suggesting retirees hold even more in fixed income to cover expenses. While some newer rules of thumb like "120 minus your age" might suggest holding up to 50% in stocks at age 70 to keep up with inflation, the core idea is the same: protect your capital above all else. These are the kinds of strategies that help ensure your savings can last for 30 years or more.

Ultimately, a well-planned asset allocation for your 60s and beyond is what turns a lifetime of savings into a durable financial engine—one that delivers security, predictability, and the peace of mind to finally enjoy the rewards of all your hard work.

Exploring Different Allocation Models

While following an age-based glidepath is a powerful and reliable strategy, it’s not the only way to build your portfolio. Think of it like a classic, time-tested recipe from a master chef—it’s solid and you know it will work. But sometimes you want something simpler, like a meal-kit delivery service, or you might want to create a custom dish that perfectly suits your tastes.

The same is true for your investments. Understanding the different approaches out there helps you land on the one that truly fits your financial personality, your specific goals, and just how hands-on you want to be. Your retirement allocation is a personal journey, and these models offer different routes to get you where you want to go.

Target-Date Funds: The Autopilot Approach

Imagine sitting down at a fine restaurant and ordering the chef’s tasting menu. Everything is planned for you, from the appetizer to the dessert, creating a perfectly balanced experience without you having to make a single choice. That’s exactly what a Target-Date Fund (TDF) does for your retirement savings.

These funds are designed to be a simple, "set-it-and-forget-it" solution. You just pick a fund with a year closest to when you think you'll retire—say, a "2050 Fund." From there, the fund does all the work. It starts aggressively with more stocks and automatically becomes more conservative with more bonds as you get closer to that target year.

- Key Advantage: The sheer convenience and automatic rebalancing make it perfect for hands-off investors.

- Potential Drawback: This one-size-fits-all approach might not be a perfect match for your unique financial situation or comfort with risk.

Risk-Based Investing: Tailoring to Your Comfort Zone

Now, let's switch from that pre-set menu to ordering à la carte, where you pick dishes based on your personal taste. This is the heart of Risk-Based Investing. Instead of letting your age call the shots, this model builds your portfolio around your personal comfort with market swings.

Financial firms often use simple questionnaires to get a feel for your risk tolerance, usually labeling you as "conservative," "moderate," or "aggressive." Each category then gets a pre-defined mix of assets.

An aggressive investor might have an 80/20 stock-to-bond mix regardless of age, while a conservative investor of the same age might prefer a 40/60 mix. This method prioritizes your psychological comfort, which is absolutely crucial for staying invested when markets get turbulent.

This approach is fantastic for anyone whose feelings about risk don't neatly align with their age. It ensures you have a portfolio you can actually stick with, preventing that all-too-common urge to panic-sell when things get choppy.

Goal-Based Investing: Aligning Assets with Specific Needs

Finally, picture yourself packing for a big trip. You'd have a beach bag for the seaside, a backpack for a hike, and a small carry-on for the flight—different bags for different activities. Goal-Based Investing works the same way by creating separate investment "buckets" for each of your financial goals.

Every goal gets its own timeline and its own asset allocation.

- Retirement (25 years away): This bucket can be aggressive, with a high allocation to stocks to maximize growth.

- Child’s College Fund (10 years away): This would have a more balanced mix of stocks and bonds.

- New Car Purchase (3 years away): This bucket would be very conservative, likely holding cash or short-term bonds to protect the principal.

This method brings incredible clarity by connecting every dollar you invest to a specific, tangible purpose. It helps you see exactly how your various life goals are progressing and makes sure you’re taking the right amount of risk for each one.

Maintaining Your Portfolio with Smart Habits

A great retirement plan isn’t something you can set and forget for thirty years. Think of your portfolio less like a time capsule and more like a well-tended garden; it needs a little care now and then to stay healthy and on the right path.

By adopting a couple of smart habits, you can make sure your retirement asset allocation by age keeps working for you. It's all about maximizing your growth while sidestepping unnecessary risks. These habits aren't complex, but sticking with them is crucial for long-term success. They boil down to realigning your investments periodically and being strategic about where you hold them to keep your tax bill low.

The Art of Portfolio Rebalancing

Imagine your portfolio is a perfectly tuned guitar. When you first set it up—say, with a 60% stock and 40% bond mix—every string is hitting the right note. But as the market plays its tune over the years, some strings get stretched. After a fantastic year for stocks, your portfolio might drift to a 70/30 mix. Suddenly, your guitar sounds a little sharp, and you’re exposed to more risk than you originally signed up for.

Rebalancing is simply the act of tuning your guitar back to its original harmony. It means selling a bit of what has done really well (the stocks, in this case) and using that money to buy more of what hasn't (the bonds). This disciplined approach forces you to sell high and buy low, pulling your portfolio right back to your target allocation.

So, how often should you do it? There are two main schools of thought:

- Time-Based Rebalancing: This is the easiest method. Just pick a date—annually, semi-annually, or quarterly—and check in on your portfolio. For most of us with a long-term view, an annual review is plenty.

- Threshold-Based Rebalancing: With this approach, you only rebalance when an asset class drifts too far from its target, usually by 5% or 10%. For example, if your 60% stock allocation creeps up to 65%, that’s your signal to tune things up.

This regular maintenance is a cornerstone of sound investing. It ensures the risk level you chose is the risk level you actually have.

The Power of Smart Asset Location

Beyond what you own, the question of where you own it is just as important. This concept is called asset location, and it’s one of the most effective—and often overlooked—ways to minimize the taxes you'll pay on your investment growth. This isn't about asset allocation (your stock/bond mix), but the strategic placement of those assets across your different accounts.

The core idea is simple: hold your least tax-efficient investments in your tax-advantaged accounts and your most tax-efficient ones in your taxable accounts.

Think of it like organizing your pantry. You put the items you use most often in the easiest-to-reach spot. With asset location, you put the investments that generate the most annual taxes (like corporate bonds or high-turnover funds) in accounts that shield them from taxes, like a 401(k) or Traditional IRA.

Here’s how that looks in practice:

- Tax-Advantaged Accounts (401(k)s, Traditional IRAs): These accounts are the perfect home for investments that kick off a lot of taxable income each year. This includes things like corporate bonds, high-dividend stocks, and actively managed mutual funds that do a lot of buying and selling. The tax-deferred nature of these accounts lets these assets grow without you having to pay taxes on them year after year.

- Taxable Brokerage Accounts: These are best for your most tax-efficient holdings. We're talking about growth stocks you plan to hold for the long haul (to get those better long-term capital gains rates), broad-market index funds, and municipal bonds (which are often tax-free anyway).

By thoughtfully placing your assets, you can give your after-tax returns a significant boost without changing your overall investment mix one bit. It’s a simple habit that helps your money work smarter, not just harder.

Of course. Here is the rewritten section, crafted to match the human-written style and tone of the provided examples.

Common Questions About Asset Allocation

Putting a plan like this into motion always brings up a few practical questions. Getting straight answers is the key to building the confidence you need to stick with your strategy for the long haul, especially when the market gets choppy.

Let's walk through some of the most common questions that come up.

How Often Should I Review My Allocation?

Think of your portfolio like an annual check-up with your doctor. You should plan to sit down and review it at least once a year. This quick check-in is just to make sure market swings haven't pushed your investment mix too far off track from your targets.

Big life events are another reason to take a look. Things like getting married, changing jobs, getting an inheritance, or seeing a child off to college can change your financial picture and goals. A review doesn't always mean you need to make changes, but it's the perfect time to ask, "Does this plan still fit our life?"

What If My Risk Tolerance Is Different From My Age?

Rules of thumb like the "120 Minus Your Age" formula are great starting points, but they're not set in stone. Your personal comfort with risk—the thing that lets you sleep at night—is just as important as any formula.

If you're naturally a more cautious person, it is perfectly fine to hold a bit more in bonds than your age might suggest. On the flip side, if you have a high tolerance for risk and a really stable financial base, you might decide to lean more heavily into stocks. The goal is to make a conscious, intentional choice that fits your personality, not to throw the whole playbook out the window.

Remember, a financial plan you can't stick with during a market downturn is a plan that is destined to fail. Personalizing your allocation to your comfort level is crucial for long-term success.

Are Target-Date Funds A Good Alternative?

For investors who just want a simple, hands-off solution, target-date funds are a fantastic option. They're designed to be a "set-it-and-forget-it" choice, automatically rebalancing and getting more conservative as you get closer to your retirement date.

The trade-off? Simplicity comes at the cost of customization. Their built-in glide path is generic and might not be a perfect fit for your specific retirement timeline or comfort with risk. They can also carry slightly higher fees than if you built the portfolio yourself using a few low-cost index funds. It really comes down to how much control you want to have.

Should My Spouse And I Have The Same Allocation?

When you're married, it's best to look at all your investments as one big household portfolio. You might have separate 401(k)s and IRAs, but you should be managing the overall retirement asset allocation by age toward a single, unified target.

This means your combined stock and bond mix should be based on your shared goals, your joint timeline, and a mutual understanding of your household's risk tolerance. This prevents one of you from being too aggressive while the other is too conservative, making sure you're both rowing in the same direction toward your financial future.

At Smart Financial Lifestyle, we believe in making smart financial decisions that build wealth and redefine what's possible for your family's future. Our approach, built on over 50 years of experience, is designed to bring clarity and confidence to your financial life. Discover more principles for lasting wealth at https://smartfinancialifestyle.com.