Are RMDs Required for Annuities? What Retirees Need to Know

Required Minimum Distributions can catch many retirees off guard, especially when annuities are involved. Understanding these withdrawal rules becomes essential for anyone pursuing tax-efficient retirement strategies. Different types of annuities follow different RMD requirements, and knowing which rules apply to your specific products helps you avoid penalties while minimizing unnecessary tax payments.

Planning withdrawals across multiple retirement accounts and annuity products requires careful coordination to meet compliance requirements without overpaying taxes. Whether you own qualified or non-qualified annuities, understanding how distribution requirements apply to each account type allows you to make informed decisions about timing and income planning. Smart Financial Lifestyle offers comprehensive retirement financial planning to help you navigate these complex rules while maximizing your retirement income.

Summary

-

Required Minimum Distributions confuse retirees because most assume annuities automatically avoid RMD rules because they are insurance products rather than traditional retirement accounts. The reality depends entirely on how the annuity is funded and owned, not the product label itself. A qualified annuity inside a traditional IRA follows the same RMD requirements as any other IRA asset because the tax treatment follows the retirement account structure, while a non-qualified annuity purchased with after-tax dollars typically carries no lifetime RMD obligations for the original owner.

-

Missing RMD deadlines remains the most expensive single mistake retirees make. Americans collectively paid over $1 billion in penalties for missed RMDs in recent years, according to The Motley Fool's analysis. Vanguard data shows that 6.7% of investors with a Vanguard-administered IRA failed to take any required minimum distribution in 2024, even though the SECURE 2.0 Act reduced penalties from 50% to 25%. The financial damage compounds quickly when distributions are delayed or skipped entirely.

-

Withdrawal sequencing across multiple account types affects retirement outcomes more than individual product selection. Two retirees with identical portfolio balances can experience dramatically different tax brackets, Medicare premium tiers, and Social Security taxation scenarios based solely on which accounts they withdraw from first. A $50,000 withdrawal from a traditional IRA creates taxable income that may trigger IRMAA surcharges, whereas taking the same amount from a Roth account or a taxable brokerage portfolio produces no additional taxable income.

-

Poor coordination between income sources creates cascading tax consequences that accumulate over decades. One poorly timed IRA withdrawal can simultaneously increase Medicare premiums for two years, raise the taxable portion of Social Security benefits, push income into higher marginal tax brackets, and accelerate future RMD obligations, all while the underlying portfolio performs exactly as expected. Each income source affects the others, yet most retirees calculate distributions in isolation rather than seeing how qualified annuity withdrawals, Social Security timing, and portfolio distributions interact.

-

Personalization in retirement decumulation has become a top planning priority according to Vanguard's inaugural How America Retires report. One-size-fits-all withdrawal approaches fail when retirees face different tax structures, guaranteed income sources, and longevity expectations. Strong retirement planning focuses on building sustainable income over 25 to 30 years while balancing taxes, healthcare costs, longevity risk, and portfolio flexibility, not just on minimizing taxes in a single calendar year.

-

Retirement financial planning addresses this by treating Roth conversions, annuity RMD strategies, and withdrawal sequencing as interconnected components rather than isolated product decisions, helping families see how their choices ripple through their entire retirement income picture across decades.

Why RMD Rules Confuse So Many Retirees

Most retirees think annuities automatically avoid required minimum distributions because they're insurance products, not traditional retirement accounts. The truth depends on how the annuity is owned and funded, not the product itself.

🎯 Key Point: The ownership structure and funding source of your annuity determine RMD obligations — not whether it's classified as an insurance product.

"The confusion around annuities and RMDs stems from the fundamental misunderstanding that product type determines tax treatment, when it's actually about account registration and funding source." — Financial Planning Association

⚠️ Warning: This common misconception leads many retirees to make costly planning mistakes when they assume their annuity will automatically provide RMD relief without understanding the underlying tax implications.

What creates confusion with annuity RMD requirements?

Two separate layers of confusion arise: the annuity contract itself and the tax classification of its account. A qualified annuity inside a traditional IRA follows RMD rules because tax treatment follows the retirement account structure. A non-qualified annuity purchased with after-tax dollars typically has no RMD requirements because taxes were already paid on the principal. Most people don't recognise these layers exist separately until after making decisions based on incomplete information.

How do misunderstandings create expensive problems?

This misunderstanding creates expensive problems down the road. Some retirees delay withdrawals entirely, believing their annuity exempts them from distributions. Others take larger withdrawals than necessary because they don't understand how annuity income interacts with broader retirement account obligations. According to Vanguard, 6.7% of investors with a Vanguard-administered IRA did not take a required minimum distribution in 2024. While the SECURE 2.0 Act reduced the penalty from 50% to 25%, missing an RMD still triggers consequences that compound quickly.

Why Multiple Accounts Multiply the Confusion

Retirees manage traditional IRAs, Roth accounts, annuities, taxable brokerage accounts, Social Security income, and pension payments simultaneously. Each account has different withdrawal and tax rules. A withdrawal strategy that looks good in one year may create higher taxes, larger Medicare premiums, or reduced portfolio flexibility if distributions aren't coordinated carefully across all these accounts.

How do you determine if your specific annuity requires RMDs?

The question "Do annuities require RMDs?" rarely has a simple answer because it depends on how you own it and how taxes treat it, not what type of product it is. The better question is: How does this specific annuity fit inside the bigger retirement income plan? That shift moves you from memorizing IRS rules to understanding how annuity taxes, account structure, withdrawal timing, Social Security income, and portfolio coordination work together across decades.

What approach helps coordinate multiple retirement income sources effectively?

The strongest retirement strategies focus less on isolated products and more on how multiple income sources work together over time. Platforms like Smart Financial Lifestyle help families over 50 map these interactions through a structured framework addressing Roth conversions, annuity RMD strategies, and generational wealth planning as connected pieces rather than separate decisions. This approach provides clarity specific to your accounts, timeline, and family goals.

The challenge is understanding when RMD rules start and what triggers them.

Related Reading

- Tax Efficient Retirement

- Can You Have Multiple Roth IRA Accounts

-

Can a Non-Working Spouse Contribute To A Roth IRA

- What Is a Tax-Free Retirement Account

- How To Reduce Taxes In Retirement

- Tax-Free Retirement Income

- Retirement Tax Savings

- What Will My Tax Rate Be in Retirement

- Do Retirees Need to File Taxes

- How to Calculate Tax on Pension Income

When Annuities Are Subject to RMD Rules

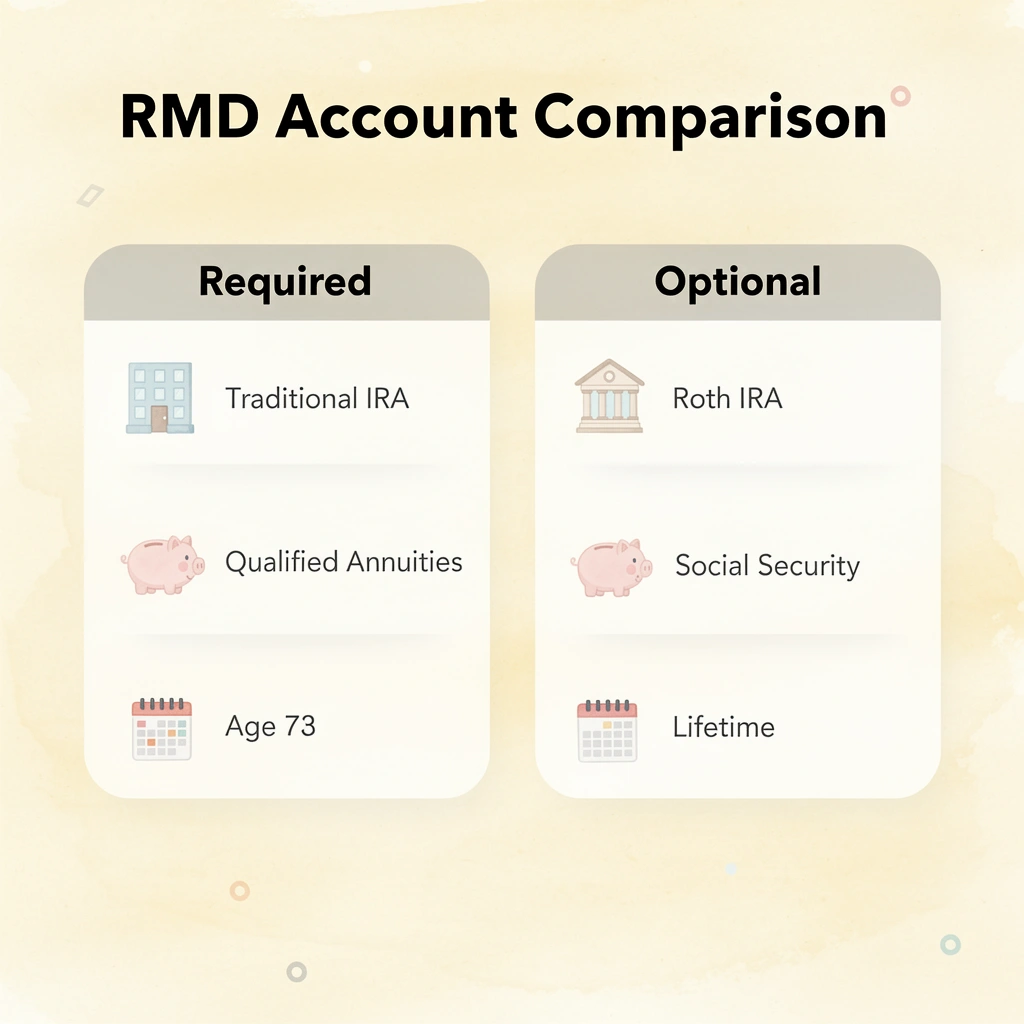

The IRS applies RMD rules based on how the account holding the annuity is structured, not the annuity contract itself. A qualified annuity inside a traditional IRA follows standard IRA RMD rules. A non-qualified annuity purchased with after-tax dollars outside a retirement account does not require lifetime RMDs for the original owner, since taxes were already paid on the principal.

🎯 Key Point: The account type determines your RMD obligations, not whether you own an annuity. Qualified accounts like traditional IRAs always trigger RMDs at age 73, while non-qualified annuities give you more flexibility.

"The account wrapper, not the investment product, determines RMD requirements for annuity holders." — IRS Publication 590-B

⚠️ Warning: Many investors mistakenly assume all annuities have the same RMD rules. Understanding whether your annuity sits in a qualified or non-qualified account is essential for retirement planning and tax strategy.

How does the funding source determine RMD requirements?

People get confused by focusing on the word "annuity" rather than its funding source. An annuity inside a 401(k) or traditional IRA has required minimum distributions (RMDs) starting at age 73 for people born between 1951 and 1959, according to current IRS regulations. An identical annuity bought with after-tax savings is not subject to those rules. The product name reveals nothing about tax treatment without knowing the funding source.

What are QLACs, and how do they affect RMDs?

Qualified longevity annuity contracts (QLACs) offer another option. QLACs allow retirees to move a portion of qualified retirement funds into a deferred income annuity, which defers RMD calculations on that amount until payouts begin, often at age 80 or 85. SECURE 2.0 expanded QLAC flexibility by removing prior percentage caps and increasing funding limits to $200,000, creating planning opportunities for retirees seeking guaranteed income later in life without forcing early withdrawals from other accounts.

When annuitization does not eliminate RMDs

Some retirees assume that converting an annuity into guaranteed income payments automatically satisfies RMD requirements. This assumption breaks down depending on payout design and IRS calculation rules. If the annuity payment falls short of the required minimum distribution calculated across all IRA assets, additional withdrawals may still be necessary. The annuity payment may count toward the RMD, but does not replace the calculation itself.

How do annuity payments affect your overall tax strategy?

When you withdraw money affects how much income tax you owe, Medicare premium brackets, Social Security taxation thresholds, and how long your portfolio will last. Our retirement planning frameworks treat Roth conversions, annuity structures, and RMD strategies as connected decisions to provide clarity specific to your accounts, timeline, and family's goals.

The challenge is understanding how qualified and non-qualified accounts, annuity payout structures, and tax-deferred retirement rules work together within a broader income strategy that preserves purchasing power, reduces tax drag, and maintains flexibility when life circumstances shift.

What makes RMD calculations more complex than expected?

Understanding when RMDs apply is only the starting point; the real complexity emerges when calculating what you owe. Our retirement financial planning resources can help you navigate these calculations and ensure you're meeting your obligations correctly.

Why RMD Planning Gets More Complicated With Annuities

Annuities don't exist in isolation. They sit alongside traditional IRAs, Roth accounts, taxable brokerage assets, Social Security income, pensions, and employer retirement plans—each following different tax rules and withdrawal requirements. Once RMDs enter the picture, retirement income planning becomes less about individual products and more about how withdrawals interact across your entire financial structure. Our Smart Financial Lifestyle approach coordinates these income sources to optimize your overall tax efficiency and withdrawal strategy.

🎯 Key Point: Managing RMDs with annuities requires a holistic view of your entire retirement portfolio, not just individual account balances.

"Retirement income planning becomes less about individual products and more about how withdrawals interact across the entire financial structure." — Smart Financial Lifestyle Approach

|

Income Source |

RMD Required? |

Tax Treatment |

|---|---|---|

|

Traditional IRA |

Yes, at age 73 |

Fully taxable |

|

Annuities (qualified) |

Yes, at age 73 |

Fully taxable |

|

Roth IRA |

No during lifetime |

Tax-free |

|

Social Security |

No |

Partially taxable |

⚠️ Warning: Failing to coordinate RMD timing across multiple accounts can push you into higher tax brackets and trigger unnecessary tax consequences.

Tax treatment creates the first layer of complexity

Qualified annuities in traditional retirement accounts create taxable distributions when you withdraw money, while non-qualified annuities only tax the earnings. Roth accounts may give you tax-free qualified withdrawals, and taxable brokerage accounts follow capital gains rules. Two retirees with identical balances can experience different after-tax results depending on the order of withdrawals: the order matters as much as the balance itself.

Withdrawal timing affects more than just your tax bracket

A retiree with a traditional IRA annuity, taxable brokerage assets, and Social Security income may face different tax outcomes depending on which accounts are used first and how distributions are spread throughout retirement. Taking larger IRA distributions earlier than necessary could increase adjusted gross income enough to raise Medicare Part B and Part D premiums through IRMAA surcharges, increase the taxable portion of Social Security benefits, or unnecessarily push retirement income into higher tax brackets.

Delaying withdrawals too aggressively can create larger future RMD obligations as account balances continue to grow. One withdrawal decision affects multiple areas simultaneously: tax brackets, Social Security taxation, Medicare premiums, portfolio longevity, and future RMD obligations.

Why is advance planning crucial even with the new RMD age?

According to NextGen Wealth, RMDs now begin at age 73, but this starting age doesn't eliminate the need to plan withdrawals years in advance. Poor coordination among annuities, retirement accounts, brokerage assets, and Social Security can inadvertently increase taxes, even when each individual account functions correctly.

Income riders versus annuitized payments add another variable

Some annuities provide guaranteed withdrawal benefits while keeping the contract value invested, while others convert fully into annuitised income streams. Tax treatment and handling of required minimum distributions differ by structure.

Why do guaranteed income payments complicate retirement tax strategy?

Guaranteed income payments don't automatically simplify retirement distributions. Coordinating them with a broader tax strategy often becomes more complicated, as a single decision can trigger multiple tax consequences at once.

Platforms like Smart Financial Lifestyle help families over 50 navigate these interactions through structured frameworks that coordinate annuity withdrawals with Roth conversions, Social Security timing, and tax-efficient sequencing strategies, compressing what once took months of trial and error into clear, actionable steps.

Even when retirees understand the complexity, they make predictable errors that cost them thousands in unnecessary taxes and penalties.

Common RMD Mistakes Retirees Make With Annuities

Missing the deadline is the most expensive single mistake. Retirees often underestimate how much time they have or believe certain annuities automatically excuse them from withdrawal requirements. According to The Motley Fool, Americans collectively paid over $1 billion in penalties for missed RMDs in recent years, reflecting widespread confusion about when distributions must begin and which accounts require them.

"Americans collectively paid over $1 billion in penalties for missed RMDs in recent years, showing widespread confusion about when distributions must begin." — The Motley Fool

⚠️ Warning: The 50% penalty on missed RMDs means that failing to withdraw your required minimum could cost you half of what you should have taken out — making this one of the most punitive tax mistakes possible.

🔑 Takeaway: Deadline confusion costs retirees millions annually because many assume their annuity provider will automatically handle RMD calculations and distributions, but the responsibility ultimately falls on the account holder to ensure compliance.

Why do people assume annuities are exempt from RMDs?

The word "annuity" can give a false sense of protection. Many retirees believe the IRS treats annuities differently because they are insurance products rather than traditional investment accounts. However, qualified annuities inside traditional IRAs follow the same RMD (Required Minimum Distribution) rules as any other tax-deferred retirement asset. The contract's structure doesn't change how the IRS classifies the account that holds it.

How do qualified and non-qualified annuities differ for RMD purposes?

Non-qualified annuities purchased with after-tax dollars are subject to different rules, which can create confusion. A retiree managing both types might satisfy requirements on one while ignoring obligations on the other, unaware that identical-looking contracts carry different tax consequences depending solely on how they were funded.

What happens when you withdraw without coordinating across income sources?

Taking only what the IRS requires ignores how that distribution interacts with other sources of income. A retiree might pull the minimum from a qualified annuity while triggering Social Security taxation thresholds, Medicare IRMAA surcharges, or pushing themselves into a higher marginal tax bracket. Each income source affects the others, yet most people calculate RMDs in isolation.

How does this damage accumulate over time?

The damage builds up over the years. A small tax problem in year one worsens across ten years of withdrawals, reducing account balances faster than necessary and limiting flexibility for future Roth conversions or strategic income timing. Our Retirement financial planning helps retirees see how qualified annuity withdrawals fit within a broader tax-efficient sequencing strategy rather than treating each account as a separate compliance task.

Misunderstanding inherited annuity rules

Beneficiaries often discover unexpected distribution requirements after inheriting retirement accounts. The SECURE Act changed how inherited retirement accounts must be distributed, including certain annuity structures, but families typically learn these rules only after the original owner dies. Relationships matter (spouse versus non-spouse), payout structures matter, and whether the annuity is qualified or non-qualified determines different timelines and tax consequences. Many heirs face unexpected taxable income because no one explained the accelerated withdrawal requirements before the inheritance.

Even perfect compliance with RMD rules can produce a flawed retirement income plan.

Related Reading

- Are Roth IRA dividends taxable

- Mega Backdoor Roth IRA

- Maxing Out Roth IRA

- Can You Tax Loss Harvest In A Roth IRA

- Annuity Vs Roth IRA

- Can RMDs be Converted to Roth

- Can a 401k Be Rolled Into a Roth IRA

- How to Reduce Taxes on RMDs

Why Retirement Withdrawal Strategy Matters More Than Individual Products

The product you choose matters far less than how you organize withdrawals across everything you own. Two retirees with identical portfolios can end up in completely different tax brackets, Medicare premium tiers, and Social Security taxation scenarios based solely on which accounts they tap first and when. The difference isn't investment performance: it's sequencing.

🎯 Key Point: Your withdrawal strategy can make or break your retirement income, regardless of how well your investments perform.

"The difference between a good retirement and a great one often comes down to withdrawal sequencing, not investment selection." — Financial Planning Research, 2023

⚠️ Warning: Many retirees focus exclusively on portfolio growth while ignoring the tax consequences of their withdrawal decisions, potentially costing themselves thousands in unnecessary taxes and higher Medicare premiums.

How do different account types affect your tax situation?

Most retirees hold money across multiple account types: traditional IRAs, Roth accounts, taxable brokerage portfolios, annuities, and employer plans. Each carries different tax rules. Withdrawing $50,000 from a traditional IRA counts as taxable income, potentially pushing you into a higher tax bracket and triggering IRMAA surcharges or taxes on Social Security benefits. Withdrawing that same $50,000 from a Roth account or taxable portfolio creates zero additional taxable income. The same withdrawal amount produces vastly different tax outcomes depending on the source.

Coordination across decades, not calendar years

Good retirement planning spans 25 to 30 years and requires balancing taxes, healthcare costs, longevity risk, and portfolio flexibility. According to Vanguard's inaugural How America Retires report, personalization in decumulation has become a top priority because one-size-fits-all withdrawal approaches fail when retirees have different tax structures, guaranteed income sources, and longevity expectations.

How do multiple retirement income sources interact?

Federal employees must coordinate several interconnected decisions: when to begin pension income, how to withdraw from their TSP, whether to use Roth or traditional accounts, which survivor benefits to elect, and when to claim Social Security. The challenge lies not in optimizing any single element, but in understanding how pension income, TSP distributions, and Social Security interact to shape your retirement tax situation.

One TSP withdrawal at the wrong time can lead to higher Medicare premiums for two years, increase taxation of your Social Security, and accelerate future required minimum distribution exposure, all while your underlying portfolio performs as expected.

What strategies work together for retirement success?

Smart planning examines how different parts work together: tax diversification keeps you flexible when tax rules change; Roth conversion planning lowers future tax liability while evening your taxable income; income smoothing strategies reduce year-to-year earnings fluctuations; liquidity management ensures access to flexible assets for unexpected expenses; estate planning determines which assets you spend first and which you preserve for heirs.

None of these strategies works in isolation; they succeed based on how well they work together with everything else happening in your financial life.

Why does coordination matter more than individual decisions?

Retirement planning is about building a system where multiple income sources, tax structures, and withdrawal decisions work together efficiently over many decades. Financial planning frameworks that address Roth conversions, annuity RMD strategies, and withdrawal sequencing as connected parts rather than separate products help retirees understand how their decisions affect their entire retirement income picture.

Being clear matters more than being fast when making long-term or irreversible decisions, especially those affecting spousal income coordination, tax brackets, and healthcare costs for years to come.

But knowing that coordination matters and doing it under real-world constraints are two different challenges.

How Smart Financial Lifestyle Helps Investors Understand Retirement Income Strategy More Clearly

Making retirement work in the real world means understanding how retirement taxes, income streams, and withdrawal timing interact over many years, not in isolation. Most retirees find financial advice scattered across the internet: articles on annuities, Roth IRAs, RMDs, and Social Security timing. Yet in real life, retirement decisions are interconnected.

🎯 Key Point: Retirement planning requires a holistic approach that considers how multiple financial strategies interact, rather than treating each income source as an isolated decision.

"Retirement decisions don't happen separately from each other—tax implications, withdrawal strategies, and income timing are interconnected elements that must be coordinated for optimal results." — Smart Financial Lifestyle Analysis

💡 Tip: Instead of researching retirement topics in isolation, understand how your Social Security timing affects your tax bracket, which impacts your Roth conversion strategy, which influences your withdrawal sequence from different accounts.

Coordination Over Product Selection

Smart Financial Lifestyle approaches retirement education differently from most product-focused financial resources. Rather than centering planning on individual financial products or isolated tax rules, we help investors understand broader principles of retirement coordination. Many retirement mistakes occur when investors optimize one area while unintentionally creating problems elsewhere: minimizing taxes today may increase future RMD exposure, maximizing guaranteed income may reduce long-term liquidity, delaying withdrawals too aggressively may create larger taxable distributions later, and poorly timed retirement income can increase Medicare premiums or Social Security taxation.

Decades of Real-World Advisory Experience

The educational perspective draws from more than 50 years of real-world advisory experience. According to Smart Financial Lifestyle, Paul Mauro spent over 50 years in wealth management and built over $1 billion in assets under management. This experience spans multiple market cycles, changing tax environments, inflation periods, and retirement transitions. Retirement income planning requires more than simple product comparisons.

Understanding Interconnected Retirement Systems

A Roth conversion affects future RMDs. RMDs affect Medicare premiums. Social Security timing affects portfolio withdrawals. Portfolio withdrawals affect taxable income. Taxable income affects long-term retirement sustainability. Effective retirement planning requires coordinating retirement taxes, income streams, account structures, and withdrawal sequencing rather than treating annuities or RMD rules in isolation.

Understanding this coordinated framework is where sustainable long-term financial decision-making begins. The real challenge is applying it to your specific situation.

Related Reading

- 403b vs Roth IRA

- Rollover Ira Vs Roth Ira

- Traditional Ira Pre Or Post Tax

- Roth Ira Alternatives For High Income

- Backdoor Roth Ira

- Tax Efficient Withdrawal Strategies

- Roth Ira Conversion Strategy

- Roth Ira Benefits And Disadvantages

- Are Rmds Required For Annuities

- How To Reduce Taxes On Rmds

- Can A 401k Be Rolled Into A Roth Ira

- Can Rmds Be Converted To Roth

-

Backdoor Roth IRA Mistakes

Kickstart Your Retirement Financial Planning Journey | Subscribe to Our YouTube and Newsletter

Applying retirement income strategy to your specific situation means asking better questions: not just whether your annuity triggers an RMD, but how that withdrawal fits into your bigger tax picture, how it affects Medicare premiums three years from now, and whether a Roth conversion this year creates more flexibility when you're 78. The difference between knowing the rules and building a sustainable plan comes down to whether you're optimizing one decision or coordinating dozens across decades.

💡 Tip: The most successful retirees don't just follow RMD rules – they integrate every withdrawal decision into a comprehensive tax and income strategy that considers Medicare impacts, Roth conversions, and long-term flexibility.

"The difference between knowing the rules and building a sustainable plan often comes down to whether you're optimizing one decision or coordinating dozens across decades." — Retirement Planning Reality

If you're trying to understand how annuities, RMDs, taxes, and retirement withdrawals fit together, explore Smart Financial Lifestyle for practical retirement income and wealth-building principles from Paul Mauro's decades of advisory experience. His books and free YouTube education content offer actionable answers specific to your situation. Subscribe to the newsletter and YouTube channel for frameworks that help families over 50 make smarter retirement decisions, execute Roth conversions, and build generational wealth.

🔑 Takeaway: Smart retirement planning requires coordinated decision-making across multiple financial vehicles – and the right education resources can help you optimize every piece of your retirement income puzzle.