How to Invest 1000 Dollars and Build Wealth Over Time

A thousand dollars is enough to start building real financial momentum. Putting that money to work is one of the most practical wealth-building habits anyone can develop, and the right approach depends on timeline, goals, and risk tolerance. Index funds, a Roth IRA, fractional shares, and high-yield savings accounts are all viable starting points worth understanding before committing.

Choosing wisely at this stage sets the tone for how money grows over the long term. Each option carries different trade-offs, and knowing those differences helps avoid costly early mistakes. For guidance on growing money steadily without needing a finance degree, retirement financial planning offers clear, practical resources from Smart Financial Lifestyle.

Table of Contents

-

Why Investing $1,000 Feels More Difficult Than It Should

-

Why Many Beginners Make Investing Harder Than Necessary

-

How to Invest $1,000

-

Why Small Investments Can Become Significant Over Time

-

Building Wealth Requires More Than Choosing Investments

-

How Smart Financial Lifestyle Helps You Build Wealth One Decision at a Time

-

Kickstart Your Retirement Financial Planning Journey | Subscribe to Our YouTube and Newsletter

Summary

-

Fear and information overload create more financial paralysis than a lack of money ever does. According to a 2025 Bank of America study, 72% of young adults take action to improve their financial health when faced with higher living costs, indicating that the desire to invest is widespread. What stops most people is the noise of competing advice, not the absence of a starting point.

-

Inaction carries a compounding cost that never appears on a brokerage statement. A $1,000 investment growing at an average annual return of 8% reaches roughly $4,660 after 20 years and nearly $10,060 after 30 years without a single additional contribution. The amount invested matters far less than when the first decision gets made.

-

Adding complexity to an investment portfolio rarely improves outcomes. Data from S&P Dow Jones Indices' SPIVA U.S. Scorecard shows that more than 79% of actively managed large-cap funds underperformed the S&P 500 over a 10-year period. If professional fund managers with full research teams cannot consistently beat a simple index, beginners who layer in more complexity are not improving their odds.

-

Sequencing matters as much as selection when deploying a first investment. Early withdrawal from retirement accounts triggers a 10% penalty on top of ordinary income taxes, which can erase months of gains in a single transaction. Meanwhile, 100% employer 401(k) matching effectively doubles a contribution before any market growth occurs, a return no index fund can reliably replicate.

-

Starting early outperforms contributing more later. A 25-year-old investing $200 a month will almost always accumulate more than a 40-year-old investing $500 a month, because time does the structural work that larger contributions try to compensate for. Small-cap equities have also historically outperformed large-cap equities by approximately 4% per year over multi-decade periods, meaning early asset allocation decisions carry real long-term consequences even at small portfolio sizes.

-

Behavior and structure drive long-term results more than investment selection does. Only 33% of Americans have a written financial plan, according to IPX1031's Investing Statistics by Generation, and the gap between market returns and actual investor returns is consistently traced to emotional decisions made during periods of volatility, not to the investments themselves.

-

Retirement financial planning addresses this by replacing reactive, open-ended research with a structured sequence of decisions tied to specific long-term goals, providing investors with a framework that remains functional even when markets make consistency feel difficult.

Why Investing $1,000 Feels More Difficult Than It Should

People hesitate with $1,000 not because the amount is too small, but because the decision feels too large. The fear of choosing wrong, losing everything, or missing a better opportunity creates financial paralysis rooted in psychology, not mathematics.

"The fear of choosing wrong, losing everything, or missing a better opportunity creates financial paralysis that has nothing to do with math and everything to do with psychology."

⚠️ Warning: This paralysis is not a sign of financial inexperience. It's a psychological trap that affects investors at every level.

According to the Bank of America 2025 Better Money Habits Study, 72% of young adults take action to improve their financial health when confronted with higher living costs. What stops most people is not laziness but the noise between intention and action — competing voices telling them to buy index funds, chase crypto, or wait for a market correction.

|

Barrier to Investing |

Root Cause |

|---|---|

|

Fear of choosing wrong |

Decision paralysis |

|

Waiting for the "right" moment |

Market timing anxiety |

|

Conflicting advice (index funds vs. crypto) |

Information overload |

|

Fear of losing everything |

Loss aversion psychology |

💡 Tip: Recognizing that the real obstacle is psychological noise — not a lack of money — is the first step toward taking action.

🔑 Takeaway: With 72% of young adults already motivated to act, the gap isn't desire — it's cutting through the competing voices to make a clear, confident first move.

Why does information overload lead to doing nothing?

Too much information is the problem. Social media, financial news, and YouTube create a constant flood of strategies, each presented as the right choice. One expert advocates low-cost index funds. Another pushes dividend stocks. A third insists on real estate or options trading. Faced with such conflicting advice, most people choose what feels safest: nothing. The irony is that doing nothing carries its own risk, one that grows quietly over decades.

Is $1,000 actually too small to be a real starting point?

The "wait until I have more" trap makes this worse. Many convince themselves that $1,000 is not a real starting point. But if $1,000 grows at an average annual return of 8%, it reaches roughly $4,660 after 20 years and nearly $10,060 after 30 years, without adding another dollar. When you start matters far more than how much you start with. Families who understand this early build wealth across generations.

Retirement financial planning built around a structured, step-by-step framework cuts through endless research by replacing open-ended deliberation with clear decision sequences: the kind of approach that has guided families managing real wealth.

What actually separates people who build wealth from those who wait?

What matters most is not finding the perfect investment, but building the habit of making decisions, following through, and staying consistent. Successful wealth builders are not people who waited for certainty; they are people who acted with sufficient information and adjusted as they learned. The first $1,000 is less about the money and more about proving to yourself that you can do this.

Related Reading

- How To Make Money Work For You

- How To Increase Net Worth

- Ways To Save Money In Retirement

-

Why Is Investing A More Powerful Tool To Build Long-term Wealth Than Saving?

- How To Save Money On A Fixed Income

- Types Of Savings Plans

- How To Build Wealth In Your 30s

- Long-term Investing

- How To Build Wealth From Nothing

Why Many Beginners Make Investing Harder Than Necessary

Beginners treat investing like a puzzle with one correct answer. The search for a perfect entry point, ideal asset, or guaranteed strategy turns a straightforward process into an exhausting loop of comparison and second-guessing. The result is delayed decisions — not better ones.

"The search for a perfect strategy is itself the strategy that fails most often — paralysis, not poor picks, is the beginner's biggest enemy."

⚠️ Warning: Waiting for the perfect moment to invest is one of the most common and costly mistakes beginners make. Markets reward action and consistency, not endless analysis.

💡 Tip: Instead of searching for a guaranteed strategy, focus on starting simple — a straightforward, low-cost index fund is almost always a stronger first move than months of comparison and hesitation.

|

Beginner Trap |

Smarter Alternative |

|---|---|

|

Searching for the perfect entry point |

Start now with a consistent contribution |

|

Chasing the ideal asset |

Build a diversified, simple portfolio |

|

Waiting for a guaranteed strategy |

Accept manageable risk and take action |

Why does research sometimes become a form of avoidance?

A new investor spends weeks comparing broad-market ETFs, individual stocks, real estate investment trusts, and cryptocurrencies. They watch tutorials, read forums, and build spreadsheets. Then the market shifts, a new opinion surfaces, and the whole process starts over. What looks like careful work is avoidance in productive disguise.

Social media speeds up the damage. Algorithms amplify dramatic wins: the person who turned $500 into $50,000, the trader who called the crash. Those stories are real, but not representative. The losses that followed, or years of failed attempts before that one win, rarely appear on the feed. According to Larry Swedroe's research published in January 2026, forecasters fail to predict market direction more than 50% of the time. The confident voices online are guessing with better branding.

How does fear of mistakes lead to costly investor behavior?

Fear of making permanent mistakes paralyzes new investors. They change strategies when markets shift slightly, or wait for a "safe" correction. This worry is understandable but costly. How investors act, not which investments they pick, drives worse results, as emotional choices push people toward buying high and selling low.

Why does adding complexity rarely improve your investing odds?

Complexity rarely improves outcomes. Owning thirty positions, rotating sectors quarterly, or timing entries around economic forecasts does not give most investors an advantage. Research from S&P Dow Jones Indices' SPIVA U.S. Scorecard shows that more than 79% of actively managed large-cap funds underperformed the S&P 500 over a 10-year period. If professional fund managers with full-time research teams cannot consistently beat a simple index, a beginner adding complexity to their first $1,000 portfolio cannot improve their chances. A structured, principle-based approach grounded in diversification, consistent contributions, and long-term thinking cuts through the noise more effectively than chasing strategies designed for someone else's situation.

Wealth built to last comes from thousands of ordinary, consistent decisions made over years without abandoning the plan when markets become uncomfortable. The principles that matter most—diversification, patience, regular contributions, and emotional discipline—are not exciting, but they work.

Once you understand what those principles look like in practice with a real $1,000, the next step becomes far less intimidating than you might expect.

How to Invest $1,000

Before investing $1,000, first assess your financial foundation — this single step determines whether index funds, retirement accounts, or other investment vehicles will create the most leverage for your money.

"The vehicle you choose for your first $1,000 can mean the difference between passive growth and maximized, tax-advantaged returns." — Smart Financial Lifestyle

💡 Tip: Always evaluate your emergency fund, existing debt, and tax situation before committing to any investment vehicle — your foundation determines your strategy.

⚠️ Warning: Skipping your financial foundation assessment is one of the most common mistakes new investors make — putting $1,000 into the wrong account type can cost you significant returns over time.

|

Investment Vehicle |

Best For |

Key Advantage |

|---|---|---|

|

Index Funds |

Long-term growth |

Low fees, broad diversification |

|

Retirement Accounts |

Tax-advantaged saving |

Tax-free or tax-deferred growth |

|

Other Vehicles |

Specific financial goals |

Flexible access and strategy |

Where your $1,000 creates the most traction

The failure point is usually sequencing. Someone skips an emergency fund, invests $1,000 in an index fund, then faces a car repair two months later and withdraws the money early. According to Forbes, early withdrawal from retirement accounts triggers a 10% penalty plus ordinary income taxes, which can erase months of potential gains in a single transaction. Getting the order right matters more than getting the investment perfect.

Why does sequencing determine whether your $1,000 actually grows?

If your emergency savings are solid and high-interest debt is behind you, retirement accounts deserve attention. Stash Learn notes that $1,000 can effectively double through 100% employer 401(k) matching, the closest thing to a guaranteed return most investors will find.

Without a structured plan, that $1,000 often ends up solving for excitement rather than impact. Families who work with retirement financial planning resources built around a step-by-step framework tend to make that first $1,000 decision as part of a larger plan, not as a standalone guess.

When investing in yourself beats the market

A $1,000 professional certification that increases your annual salary by $8,000 produces a return no brokerage account can reliably match. Broad index funds are powerful over decades, but your earning capacity is the engine that funds every future contribution.

Self-investment and market investment work in sequence. Build your income, then direct more of it into low-cost, diversified index funds through tax-advantaged accounts. The habits, account structure, and decision-making framework you establish around investing will determine your financial life in twenty years.

That first small, consistent decision compounds into something that feels almost impossible to explain.

Why Small Investments Can Become Significant Over Time

Small investments become significant over time because of compounding's geometric growth. The early years appear quiet; the later years become impossible to track without a spreadsheet.

"The most powerful force in the universe is compound interest — the engine that turns small, consistent investments into extraordinary long-term wealth." — Financial Planning Principle

💡 Tip: Don't judge your investment progress by year two. The real gains build in years ten, fifteen, and twenty.

Most people quit during this quiet early phase, overestimating year-two gains while dramatically underestimating year-twenty results. The portfolio feels stagnant, contributions feel trivial, so they stop or switch strategies — and that decision is enormously costly. They miss that compounding builds geometrically — the acceleration only becomes visible after years have passed.

|

Phase |

What It Feels Like |

What's Actually Happening |

|---|---|---|

|

Years 1–3 |

Slow, discouraging |

The foundation is being built |

|

Years 5–10 |

Modest progress |

Momentum is compounding |

|

Years 15–20+ |

Explosive growth |

Geometric acceleration kicks in |

⚠️ Warning: Switching strategies during the early quiet phase is one of the most common — and most damaging — mistakes investors make. Patience is not optional; it's the strategy.

🔑 Takeaway: Compounding rewards consistency above all else. The investors who win are not the ones who found the best shortcut — they're the ones who stayed in long enough to let geometry do the work.

Why does early asset allocation shape long-term outcomes?

According to Wellington Management, small-cap stocks have historically outperformed large-cap stocks by about 4% per year over decades at current valuation levels. Over twenty or thirty years, that difference compounds significantly. Early asset allocation decisions have substantial long-term effects.

What separates investors who build real wealth from those who don't?

Most people treat their first investment as a test, watching it closely and evaluating its results over the next 12 months. The first investment is not a test: it is the anchor point for every contribution, reinvestment, and compounding cycle that follows.

Paul Mauro spent more than five decades observing families build real wealth, and found that success depended not on which stocks they picked, but on how early they started and how long they stayed. Frequent reassessment often triggers emotional decisions at exactly the wrong moments, interrupting the compounding cycle before it gains speed. Resources like the retirement financial planning framework at Smart Financial Lifestyle replace that reactive pattern with a clear, repeatable process that keeps long-term investors from getting in their own way.

Why does your age matter more than your investment amount?

The size of your first investment matters far less than the age at which you make it. A 25-year-old investing $200 a month will almost always outperform a 40-year-old investing $500 a month, despite the older investor contributing more than twice as much monthly. Time accomplishes what larger contributions cannot. According to Wellington Management, small-cap stocks currently trade at roughly a 20% discount to large-cap stocks on a forward price-to-earnings basis, near historically wide levels, offering long-term investors willing to hold through volatility an unusually attractive entry point.

What should the real goal of a first investment be?

The goal of any first investment should be to build the habit, set up the account structure, and let time compound. Small amounts become significant through consistent action over years, not luck or perfect timing.

But here is what most investors never consider: choosing the right investments is only part of the equation.

Building Wealth Requires More Than Choosing Investments

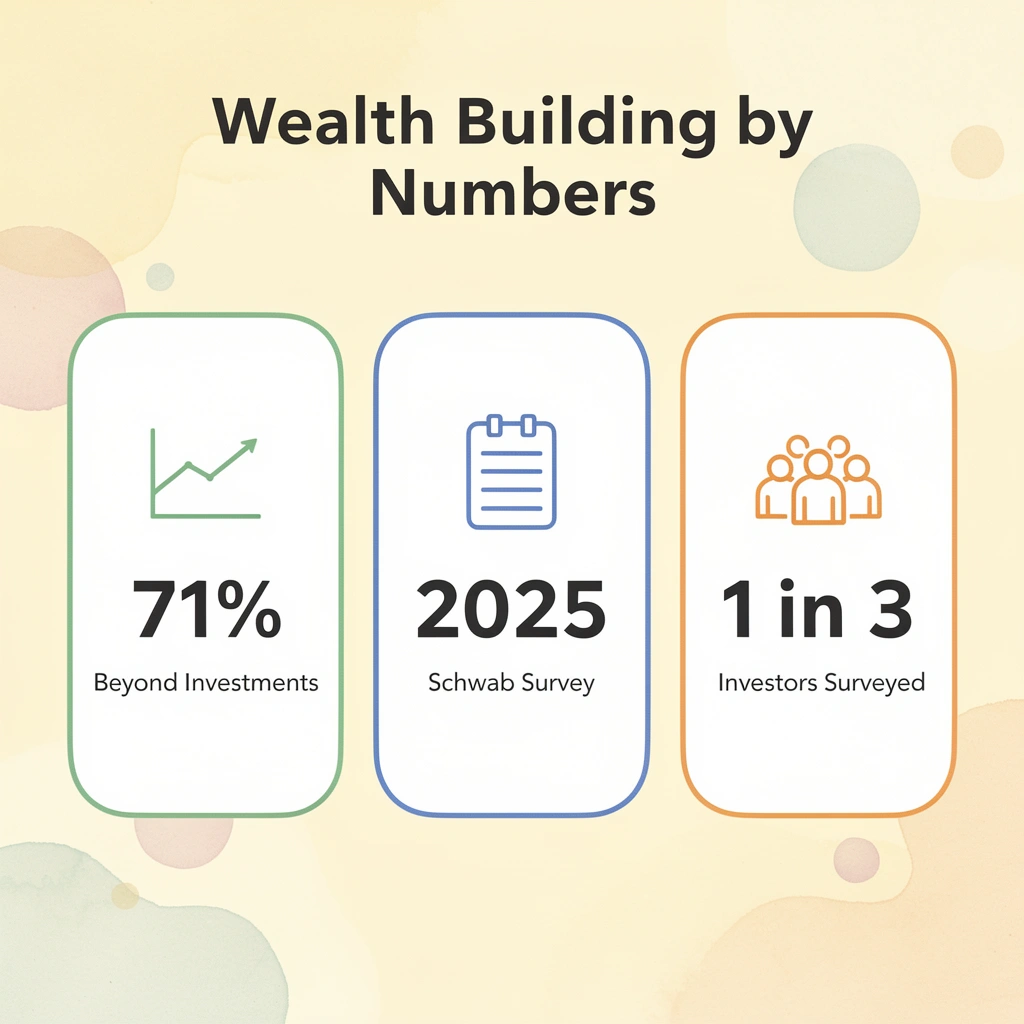

According to the Charles Schwab 2025 Modern Wealth Survey, 71% of investors say that building wealth requires more than picking the right investments. Success depends on how you act, how you organize your money, and the discipline to stay consistent, even when markets make it feel impossible.

"71% of investors say that building wealth takes more than just picking the right investments." — Charles Schwab 2025 Modern Wealth Survey

🔑 Takeaway: Investment selection is only one piece of the puzzle. Behavior, organization, and consistency are equally critical drivers of long-term wealth.

💡 Key Insight: The majority of investors already recognize that financial discipline and structured money habits matter as much as which assets you choose to hold.

What actually drives long-term results?

The failure point is usually not the investment itself, but the investor's response to what happens after. DALBAR's research on investor behavior shows that the gap between market returns and actual investor returns stems from emotional decisions: buying after markets rise, selling after markets fall. Over decades, this pattern compounds into a meaningful shortfall that no single great investment can overcome.

Why does asset allocation matter more than picking the right stock?

Asset allocation deserves more attention than most beginners give it. The mix of stocks, bonds, and other assets across different industries, geographies, and risk profiles shapes long-term results more than any individual security selection. Someone with 30 years until retirement can handle volatility that would hurt someone five years out. Getting that mix right and adjusting it as life changes is the structural work most investors skip because it feels less exciting than picking the next winner.

How does a written financial plan change investment outcomes?

Most people plan for their financial future informally, reacting to situations as they occur without writing anything down. According to IPX1031's Investing Statistics by Generation, only 33% of Americans have a written financial plan. A written plan tied to specific goals—retirement, education funding, a home, financial independence—gives every investment decision purpose and direction. Without it, even good investments lose focus. Families who work with retirement financial planning resources built around a structured framework stay on track more easily because the plan exists outside their emotions.

When does wealth preservation become the priority?

The strategies that build wealth differ from those that protect it. As assets grow, the focus shifts toward tax efficiency, estate planning, and protecting purchasing power from inflation. Paul Mauro spent more than five decades advising families managing over a billion dollars in assets and observed a consistent pattern: investors who preserved generational wealth were not those who found the best stocks, but those who built systems around discipline, diversification, and a clear sense of what the money was ultimately for.

Wealth built without legacy intention remains transactional. Wealth built with it becomes something worth protecting, passing on, and teaching. That shift in purpose changes every decision that follows.

Knowing all of this is only the beginning of what it takes to act on it.

Related Reading

- Passive Income For Retirement

- How To Maximize Retirement Savings

- Wealth Creation Plan

- How To Catch Up On Retirement Savings In Your 50s

- Long-Term Financial Planning

- How To Grow Your Money

- How to Stop Living Paycheck to Paycheck

- How Much Money Should I Have Saved by 30

How Smart Financial Lifestyle Helps You Build Wealth One Decision at a Time

After learning how to invest $1,000, many people face a bigger question: "How do I continue making smart financial decisions over the long term?" Building wealth requires far more than choosing investments — it demands discipline, patience, and principles that guide decisions through changing markets and life stages.

"Building wealth is not a single decision — it's the compounding result of hundreds of small, disciplined choices made consistently over time." — Financial Planning Principle

🎯 Key Point: Long-term wealth isn't built overnight — it's the product of consistent, principled decision-making applied across every stage of your financial life.

💡 Tip: Start by anchoring your finances to core principles — discipline, patience, and a long-term mindset — before focusing on specific investment tactics.

|

Wealth-Building Pillar |

Why It Matters |

|---|---|

|

Discipline |

Keeps you on track when markets are volatile |

|

Patience |

Allows compound growth to work over time |

|

Guiding Principles |

Ensures consistent decisions across life stages |

Who is behind Smart Financial Lifestyle?

Smart Financial Lifestyle centers on Paul Mauro, whose 50+ year career in wealth management included managing over $1 billion in assets and guiding clients through bull markets, recessions, retirement planning, and wealth preservation.

A key lesson from those decades: successful investing stems from consistent habits and sound principles, not market prediction or shortcuts. Wealth is built one decision at a time.

What wealth-building resources does Smart Financial Lifestyle offer?

Through his books, Paul shares wealth-building ideas previously available only to premium clients who paid thousands for professional advice. Rather than focusing on speculation or forecasts, the material emphasizes timeless principles that work regardless of market conditions.

Smart Financial Lifestyle offers free YouTube content covering long-term investing, retirement planning, asset allocation, risk management, wealth preservation, behavioral finance, and financial discipline.

Why does investor behavior matter more than market conditions?

This focus on behavior is particularly important. Markets fluctuate, and uncertainty persists, but investors who understand how emotions influence decisions are better prepared to stay disciplined and avoid costly mistakes.

Instead of encouraging constant trading or trend-chasing, Smart Financial Lifestyle helps people develop the mindset needed to build and preserve wealth over decades, creating lasting financial security through informed decisions and sustainable habits.

Kickstart Your Retirement Financial Planning Journey | Subscribe to Our YouTube and Newsletter

Understanding what to do is one thing; building the habit of doing it consistently across decades separates those who retire with options from those who retire with regret. If you're ready to move from understanding to action, explore retirement financial planning with Smart Financial Lifestyle. Our retirement planning approach teaches the wealth-building principles Paul Mauro applied across a 50-year career advising families with over $1 billion in assets, covering long-term investing, risk management, and how to build wealth through consistent decisions rather than shortcuts.

"The same wealth-building principles applied across a 50-year career advising families with over $1 billion in assets are now available to everyday investors through Smart Financial Lifestyle." — Smart Financial Lifestyle

🎯 Key Point: Consistency over decades—not one-time decisions—separates a comfortable retirement from a regretful one.

⚠️ Warning: Relying on shortcuts instead of proven, long-term wealth-building principles is one of the most common mistakes retirement savers make.

Subscribe to the Smart Financial Lifestyle YouTube channel and weekly newsletter to keep those principles front of mind as your portfolio grows. The free 5-step wealth-building checklist is a perfect starting point if your first $1,000 is already invested and you're asking what comes next.

💡 Tip: Use the free 5-step wealth-building checklist as your immediate next action — it's designed for investors who have their first $1,000 invested and are ready to build serious momentum.

|

Resource |

Best For |

Format |

|---|---|---|

|

YouTube Channel |

Visual learners & ongoing education |

Free video content |

|

Weekly Newsletter |

Keeping principles top of mind |

Free email digest |

|

5-Step Wealth-Building Checklist |

Investors with the first $1,000 invested |

Free downloadable guide |

Related Reading

- Low Risk Investment Options

- Early Retirement Strategies

- How To Grow Your Money

- How Much Should I Save Each Month

- What Happens If You Run Out Of Money In Retirement

- Retirement Income Strategies

- Long-Term Stock Investments

- Retirement Planning Mistakes

-

Best Investment For Retirement Income

- Are Index Funds Good For Retirement

-

Ira Pros And Cons